Skip to content

Skip to content

The Magic of Compound Interest

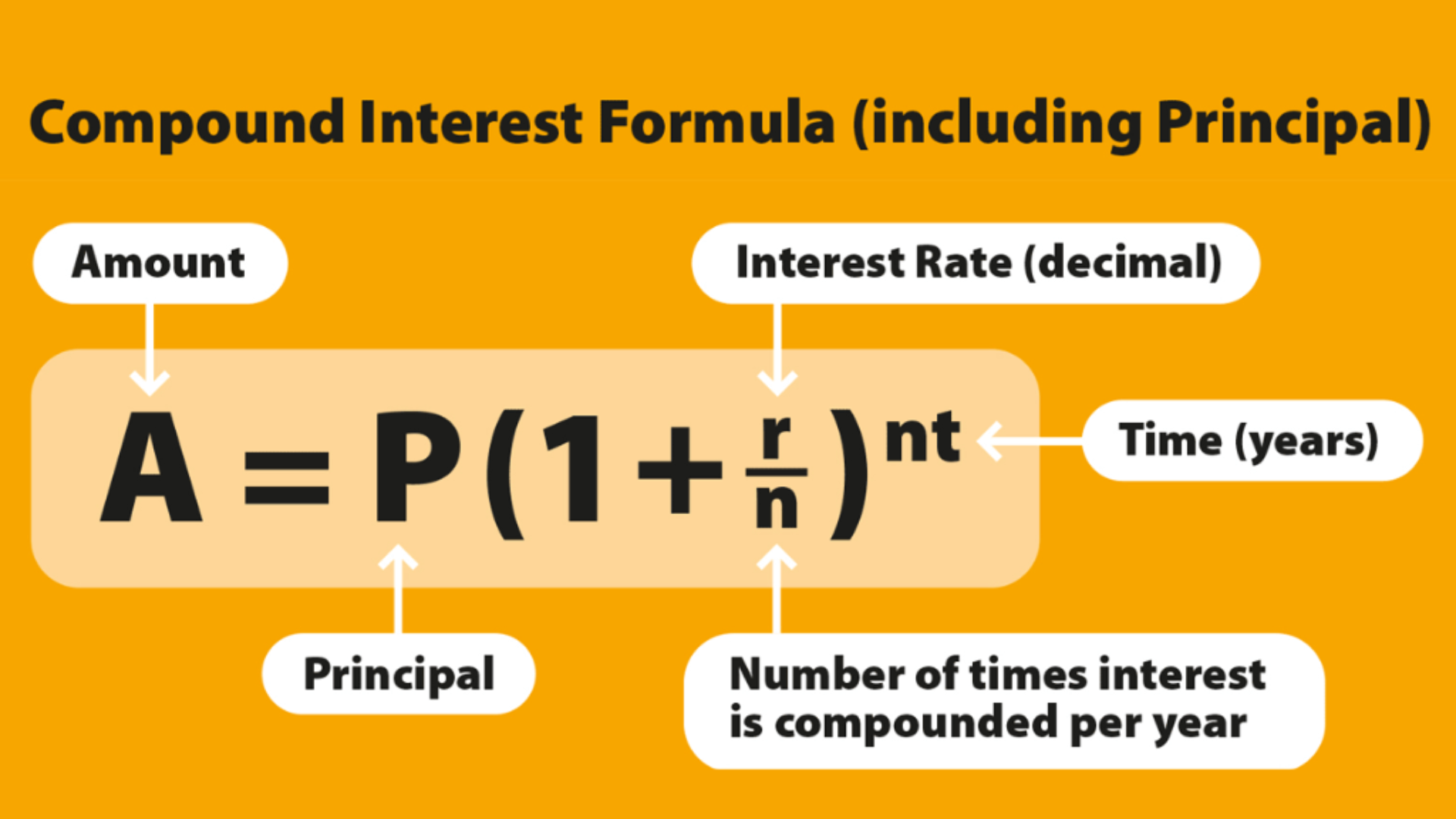

You may have seen the above formula for compound interest in your schools and mathematics textbooks. Remember? Those laborious test sheets determining the answer to problem statements and mathematical problems are hard to forget.

Then you might not have understood the power of compound interest, but you sure would want to learn now.

Often referred to as EIGHTH WONDER of the world. Compound interest is the foundation of your financial success.

If you do not bring your head around this phenomenon, it is hard for you to gain any financial wisdom and, ultimately, the financial freedom you seek.

The fundamentals of compound interest defy the usual linear thinking of humans.

E.g.

You would be able to answer the following expression:

8+8+8+8+8+8+8+8+8

You need to add on 8, and that’s it.

But when the expression changes to:

8x8x8x8x8x8x8x8

You wouldn’t be able to process it without any calculator, provided you yourself are not a calculator. 🙂

By learning about the compound interest you not only make better financial decisions but also prevent yourself from making blunders like many others and ultimately sinking into the debt trap.

In your effort to be financially free, you will have to learn about its fundamentals.

Effects Of Compound Interest:

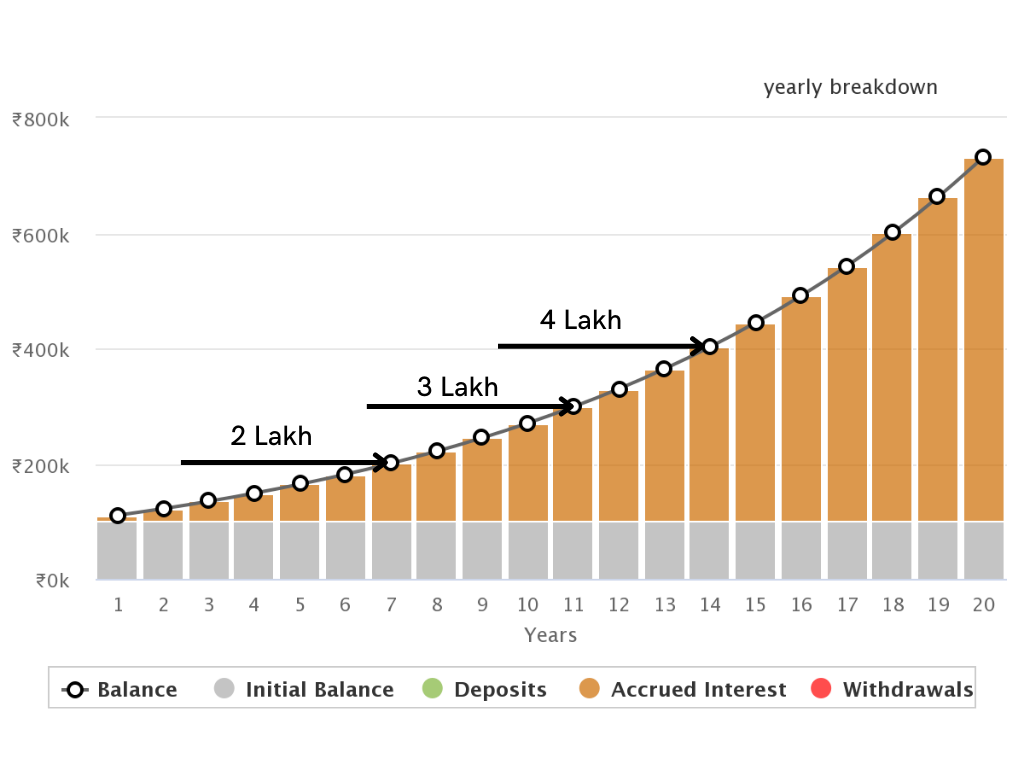

Before diving in to the theory about the compounding, let me demonstrate to you the effects of compounding pictorially.

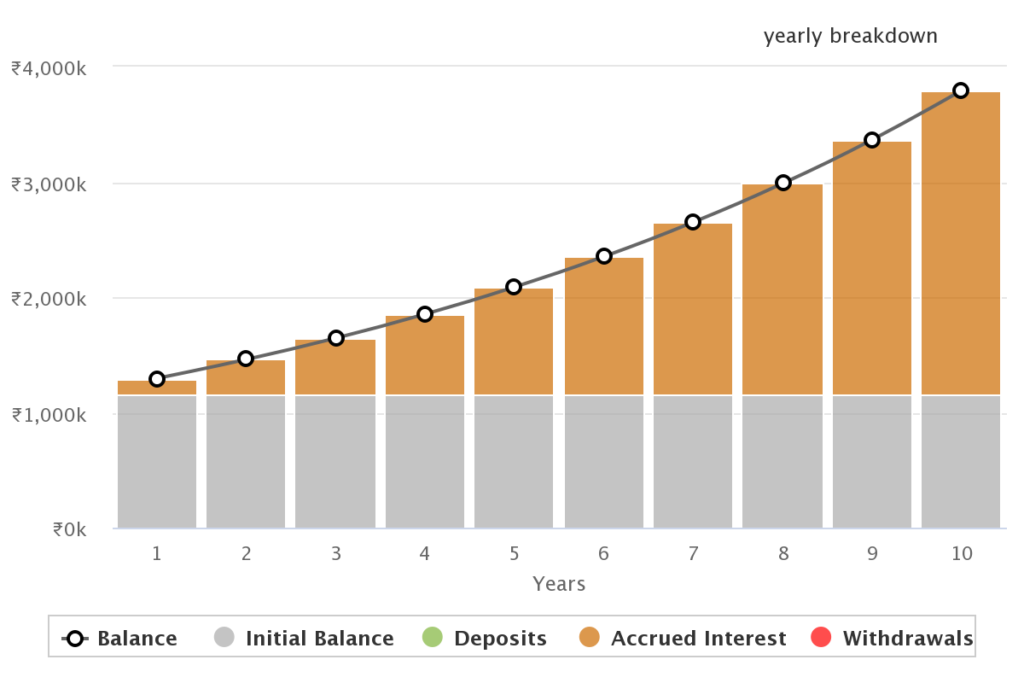

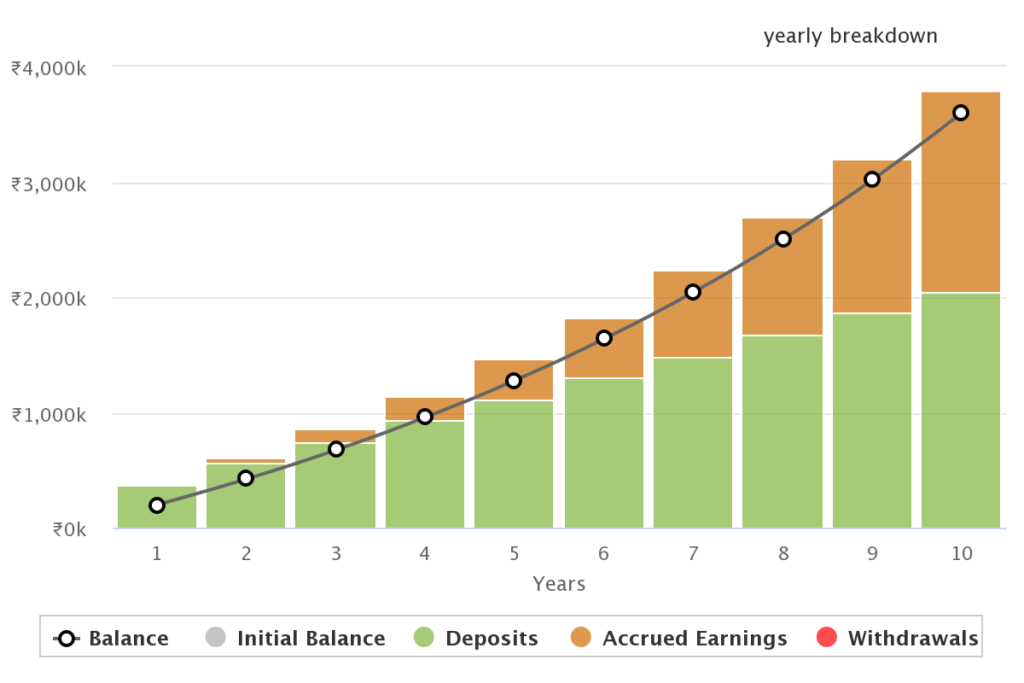

Let’s say you save a corpus of 1 lac rupees and invest it for the long term in an instrument giving you 10% interest per annum.

For you to earn additional 1 lac rupees to take your final amount of 2 lac rupees, it will take you roughly 7 years.

Seems a bit long isn’t it.

But here comes the crucial part, this time the duration it takes to earn the next 1 lac is not 7 years, but only 4 years.

And for the next, only 3 years. This is how your money gets multiplied quickly, again and again, to grow your money continuously.

The multiplication of money at such a rapid pace is incomprehensible. It is because our brains are wired to have linear thinking and are not shaped to think such exponential calculations. That is why compound interest is often referred to as EIGHT WONDER. This is how your money grows over a long duration of time.

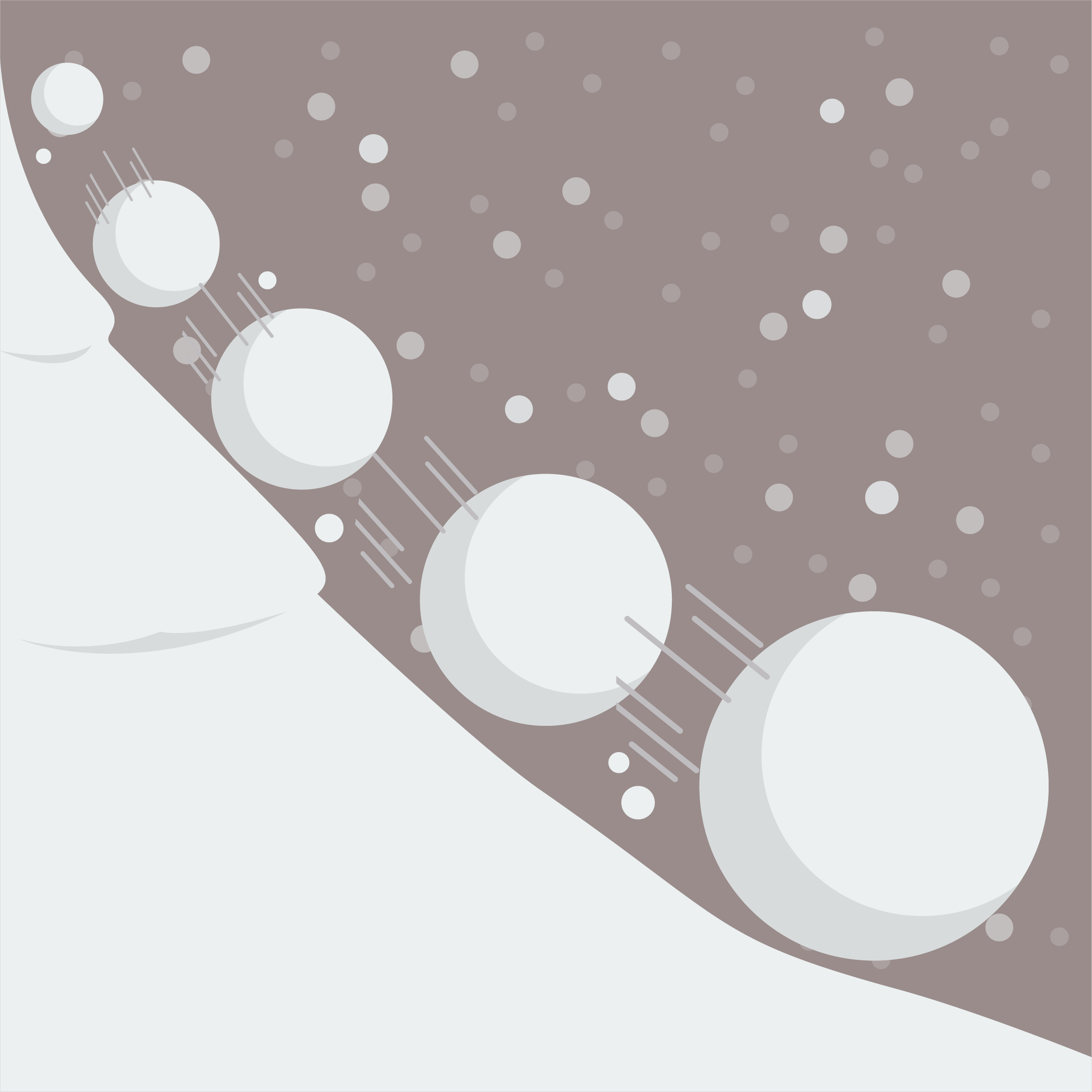

Let us understand the analogy of the effect of compounding with the snowball effect.

Snowball Effect

What happens when a tiny snowball is pushed down a hill… What relevance does this have to become wealthy, then?

A little snowball continuously gathers snow when you roll it down a slope. It is a massive snow boulder when it reaches the bottom of the hill.

As it rolls down the slope, the snowball gets bigger. The more snow it adds with each rotation, the bigger it gets.

Compounding is represented by the snowball effect. It demonstrates how little things are done repeatedly and can have a large impact.

The interest you earn gets added on to the principle and in turn starts accruing more interest. And in no time your amount grows bigger and bigger.

Application of Compound Interest: The Desire of Financial Freedom

Everybody wants to live a happy and meaningful life. Much of which is satisfied by having a certain amount of currency in your pocket.

You must have heard that money can not buy happiness, but not having money can surely invite sorrow and pain. Due to this and many more prevailing reasons, it is necessary to save money for your future, and that too on time.

You can save money and even let them earn more using investing. Where you invest is your choice. Investing is crucial in the endeavor to become financially free.

When you put money in an asset designed to give you money in the future, you not only save money by limiting your unwanted expenses today but also create an income stream for your future self when you put the earned money to good use.

A detailed article on the importance of investing is provided below.

Before proceeding further, I urge you to kindly read the above article as it would cement my argument of encouraging you to invest.

The assets you decide to put your money in are your independent choice.

As investing in the stock market is the usual choice, I would base my following article on the stock market itself. The stock market is the platform where you buy and sell shares of listed companies offering various services.

E.g.

In India, Reliance Industries is one of the giants, and you can buy or sell its shares. When you possess shares of certain companies, you become their part owners. Similarly, you can buy shares of Apple, Amazon, and Tesla to ride along with their success.

You can choose to invest in India Or US stocks which have their own merits as a part of a diversification plan giving you better results.

Note: No Rewards shall be applicable without referral code

How To Use Stock Market To Gain Financial Freedom:

If you are in your early 20s and are interested in the financial world and personal finances, I am sure you must have started investing whatever you can in stocks and mutual funds.

Mutual funds are the baskets of stocks giving the results as the companies perform. If the companies perform well, their share prices go up, similarly, the mutual fund goes up and vice versa.

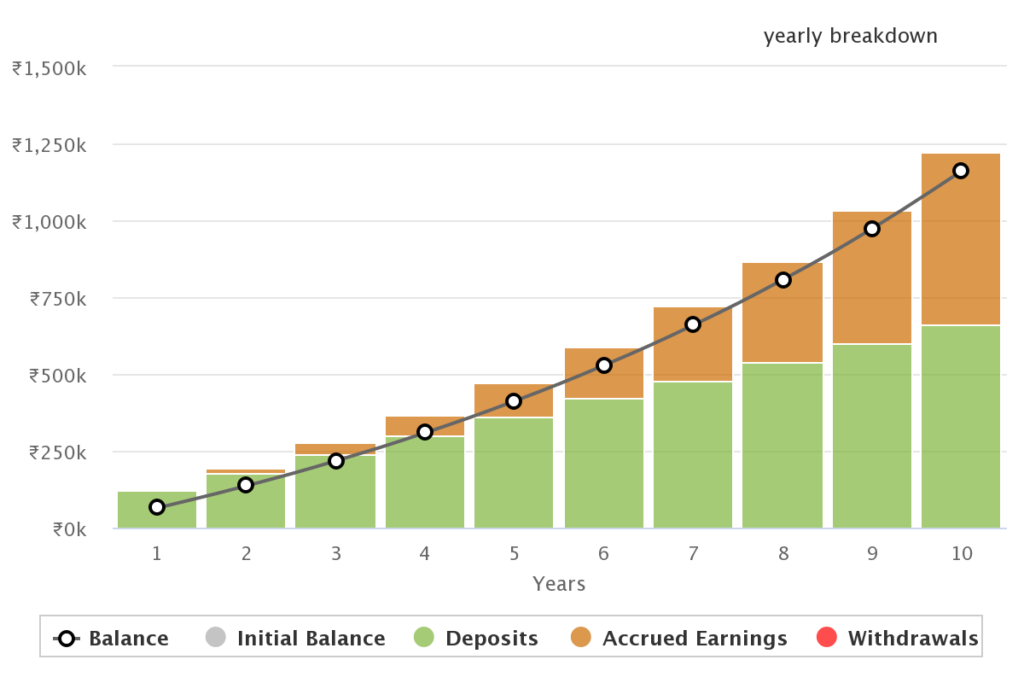

Let’s say you invest Rs 5000 every month in Indian Index Funds giving you a 12% annual return when you are 20 years old.

Let’s assume you will only invest it for 10– years.

After 10- years, when you reach age 30, you would have invested:

Rs 5000 (per month) *12 (months in a year) *10 (investment duration)= Rs 6,00,000.

Can you guess your amount after 10– years?

It would be 11,50,000.

Try out the SIP calculator Yourself.

Now should you decide to stop investing and let the money grow in the same fund for the next 10- years, and when you reach the age of 40, the same money will grow to 35,71,000.

How a monthly investment of Rs 5,000 for 10- years changed to 35.71 Lacs is beyond our thinking.

Time Factor: A Crucial Element For Success In Compounding

Till now, you only know the half magic of compound interest. The rest lies in the power of the period.

Considering the similar example as the previous one, let’s say you start a little late and then start investing at age 30. Considering the same investment plan giving a 12% annual return, do you know how much you need to invest monthly to get to the same corpus of around 35.5 Lacs?

The calculation comes out to Rs 15,500 a month.

But that is not all. This time you will be investing around 18 lacs to receive the corpus of 35.5 lacs at age 40, whereas in the previous case, you only had to invest Rs 6 lacs.

ONE-THIRD of what you invested now if you start 10- years early.

That is why you must have heard so often to start investing early.

The above point is not to tell you to invest all your money now only, the emphasis is on developing your investment strategy and discipline. Whatever remains after a certain period should better be invested in well-researched investment opportunities, rather than just leaving it as it is.

"The Psychology" Of Investing

In this section, I will paraphrase an excerpt of The Psychology of Money, describing what happens when you invest earlier than most people.

This story involves two legendary investors,

Warren Buffet and Jim Simons.

It goes like this

Buffet began serious investing when he was 10- years old. By the time he was 30, he had a net worth of $1 Million. His net worth today is $84.5 Billion.

Let’s say he started at age 30 and still gave the same annual returns of 22%.

Then at age 60, his net worth would have been 99.9% less at $11.9 million.

Effectively all of Warren’s success can be tied to the financial base he built in his pubescent years and the longevity he maintained in his long years.

His skill is investing, but his secret is time.

Another hero in our story is Jim Simons, who started investing at the age of 50 years. But the result he gave were mindboggling. He produced an annual return of 66%, giving him a net worth of only $21 Billion. 75% less than Warren.

If Simons had earned his 66% for the 70 years duration, which is as long as Warren’s, he would be worth:

Sixty-three quintillion nine hundred quadrillion seven hundred eighty-one trillion seven hundred eighty billion seven hundred forty-eight million one hundred sixty thousand dollars.

These are ridiculous, impractical numbers. The point is that what seems like a slight change in growth assumptions can lead to ridiculous impractical numbers.

Bonus:

You know there exists a sibling of compound interest involved in the picture when you make monthly investments, like the one we gave an example of at the beginning of the article. The use cases are different, that is why you need to learn this feature as well.

The method is referred to as XIRR or Extended Interest Return Rate:

Let me explain this concept. Suppose you invest 10,000 rupees each month for 12 months, and at the 13- month, you see your portfolio and see your returns.

Whatever the return may be.

Now, if I ask you, did each investment contribute to the return equally? The answer will be a definite no.

Your first month’s investment earned money for you 12 months, while the last month’s payment only earned you money for less than a month.

So how can you determine what your overall return has been?

Here comes the XIRR into the picture.

It gives you the actual return of your overall money invested and, at the same moment takes into account the contribution of individual investment according to the time invested.

Want to know how to calculate the XIRR. Click the video below.

Recommended Books:

Conclusion:

I hope that you were able to understand the beauty of compound interest and apply the knowledge to your financial planning.

To gain more knowledge regarding the finance world I encourage you to read the books mentioned in this article and have a well-built financial success.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.