Skip to content

Skip to content

How to Invest 1 crore rupees

Have you ever wondered what you would do when you earn a large sum of money or when you are made responsible for investing a large sum of money for yourself or your loved ones? In this article, we will talk about the ideal approach for the general audience and better understanding. We will focus on how to invest 1- crore rupees. You may get your hands on an amount more or less than the amount used in this article, but more or less, the theory behind the investment is the same.

Let's begin.

Before deciding the investment strategies, there are a few questions that you have to answer:

- What is the purpose of your investment?

- What is your risk appetite? How much risk you are willing to take for future growth?

- What is the time horizon for investment?

- Do you have any other income source, or whether you rely on this amount only for meeting your financial needs?

Knowing the answers to these questions will help you understand your financial needs.

Let’s start the investment journey.

When you begin the investment planning, ensure one thing: You have your emergency funds ready.

Emergency funds are necessary as they help in some unwanted and unimagined financial situations and prevent you from disturbing your investments.

If you have the funds, well and good. Otherwise, keep aside some funds from this corpus for this purpose.

Don’t know how to create your emergency fund? Check out our article on building an emergency fund for yourself.

Allocation of funds:

Now comes the part of allocating the funds. There are essentially two main instruments that we will lay our hands on, which are Equity and debt.

You may have reservations about these instruments, but these are the best assets for a general audience. You can check some of our articles discussing the advantages of investing in these instruments in our portfolio.

The standard application for an equity investment is for future growth. Our investment compounds over a period, giving better returns. Equities are a risky investment, and it takes time to mature. If you invest for 1-2 years, you might not get the result, but if left alone for 10-12 years, you are more likely to earn a reasonable sum.

We have added bonds to our portfolio to meet short-term needs and increase the cash flow.

How you choose between the two depends on the age group you are and the dependency on the funds.

Join our Mailing list!

Get all latest news and updates.

Let’s say a 25-year-old working individual would not depend on this investment. He can invest 80% into equities and the remaining in debt as a balanced investment approach. But a person of the same age but not employed might have to rely on the income from bonds, so he might only invest 40% in equities and the rest in bonds.

Similarly, a person aged 50 might not want to take high risk in equities as they take time to mature, and any person at this age would prefer enjoying the money now than to wait for 10- years. For them, 80% debt and 20% equities make much more sense if they still earn. But people who have retired at the same age will be safe by investing 90-95% in bonds and the rest in equities.

To sum up, your decision will depend on:

- Long-term and short-term needs.

- Your age

One thing I wish to state is that it is not necessary to invest in only these 2- assets. I am only discussing these two assets as these are more readily available. You might come across a more lucrative option. You weigh the pros and cons and decide what’s best for you.

The Returns:

Let’s discuss the standard 80-20 investment strategy. Eighty percent to be invested in equities, and the other portion is in debt.

Let’s choose the simple instrument in equities, i.e. the index fund.

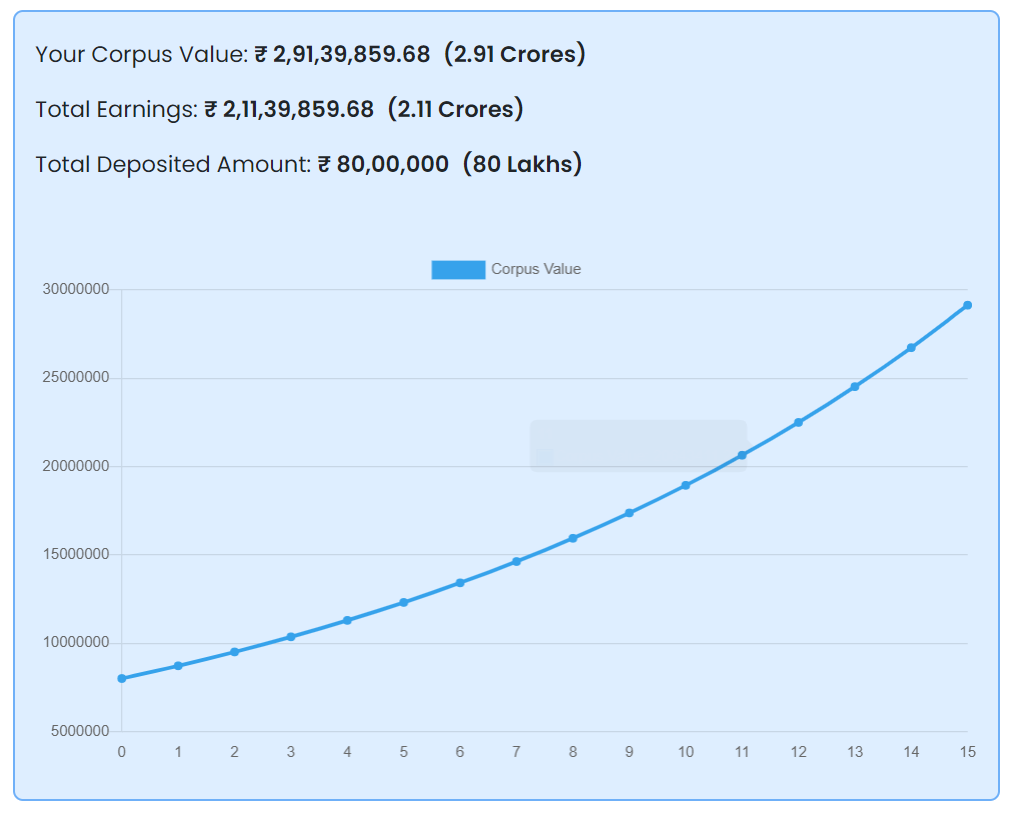

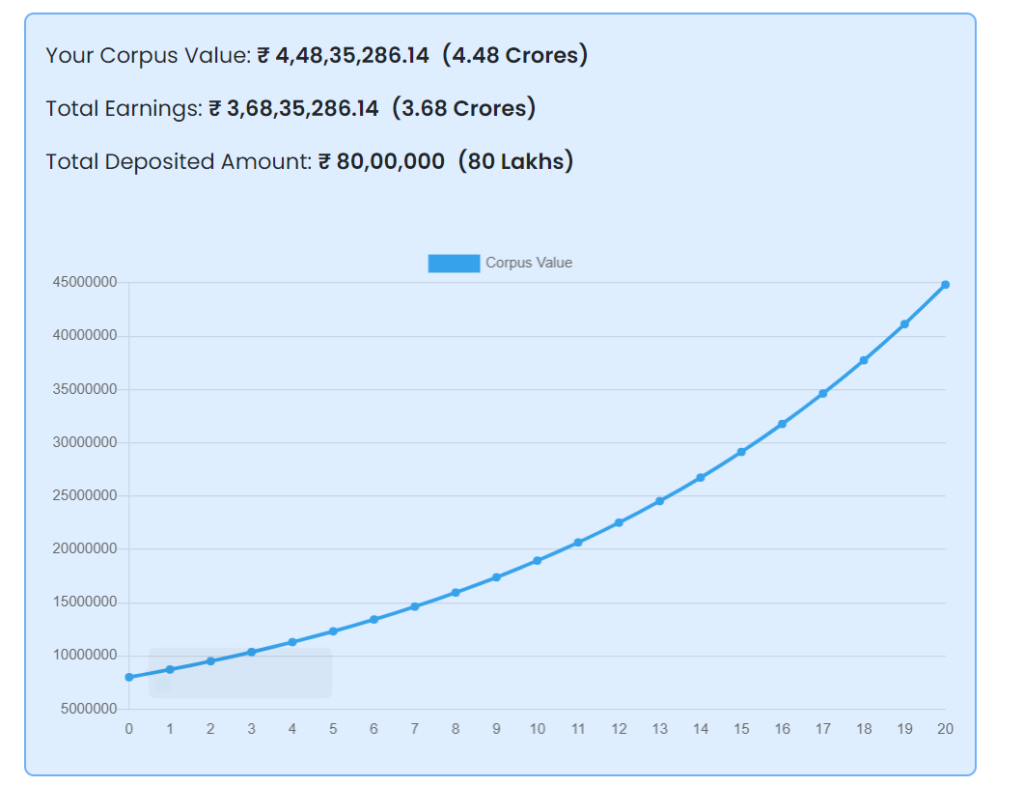

The past return of an index fund has been somewhere between 11-13%. Let’s be conservative and assume it gives a 9% return from this point forward.

Look for any lumpsum investment calculator and see the growth in 10, 15, and 20 years.

Decide what horizon you are looking for and how much you want to fulfill your needs and goals in the future.

The Debt Portion:

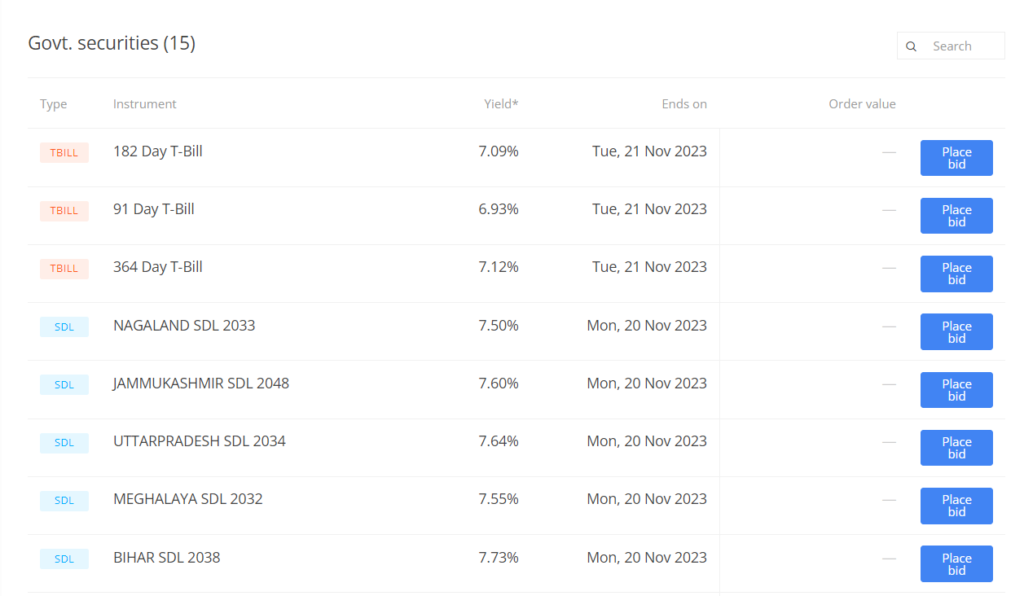

We kept aside 20% or 20 lacs for investment in debts. It can be of various types, but we will choose one of the simple and previously discussed debts: Government Securities.

If you see the current bond offered by the Government of India, you can see bonds of different coupon rates. Let’s choose the one with a 7% interest rate.

If you invest 20 lacs in it, you will receive 1.4 lacs annual interest for a very long period. If you do not touch it for the whole tenure, you will keep receiving the money at no extra cost.

This extra payment can help you meet short-term needs and arrange money if anything spontaneous comes up.

It is better to increase this portion if you feel you require more support as regular income.

Final Words

Investment in any instruments should be made after understanding your financial needs and future goals. Remember that if you do not need to touch any money for any foreseeable future, you could invest it in equities, especially index funds, but if you have any upcoming expenses then it is better to move it towards bonds.

P.S. If you want to read more about how to better manage your money, I would advise you to read Let’s Talk Money by Monika Halan. You’ll be able to learn great things from it.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.