Skip to content

Skip to content

How to start investing in your 20s in India

The finest advice anyone can ever give you is to start investing in your 20s because it is the perfect age to start. You begin to see the value of saving, investing, and returning in your twenties. At this age, you take a step towards gaining financial independence and gradually assume responsibility for your own life.

The most valuable factor is that time, which is more advantageous than money in investing, is the most crucial resource.

Therefore, if you intend to begin your investing career in your 20s or wonder how to start investing in your 20s, this blog is just for you! Read on to know more.

Know your investment objectives:

The whole objective of money is to buy/ experience things you want. Money in itself does not do anything. It just sits there. So before you begin your investment journey, you must map out your objectives of what you want to do with whatever money you earn.

No doubt, the objectives will change as you age, but those will be gradual changes, some anticipated, others entirely unexpected. You can always include the expected change in your plan and consider some buffer.

So, to have an idea of how to create a layout of your money needs, head out to this article:

Meet Your Investment Objectives

In the above-said article, you will become familiar with the steps and ideas to plan your money goals.

Once you have outlined goals and established a plan, you’ll be ready to look into the assets to invest.

Utilizing the early years:

The greatest gift you can ever give your future self is early investing. There is a strong reason why early investing is favored. And that is due to the power of compounding.

You can also call it the eighth wonder of the world. If you understand the significance of this formula, you’ll never remain poor.

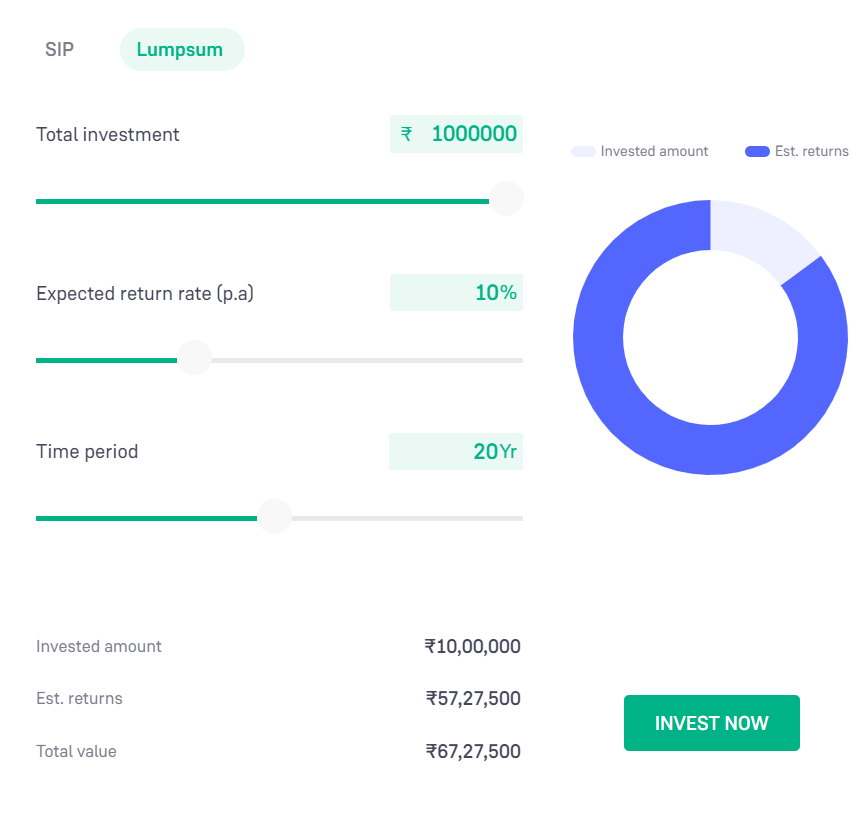

Consider a 10lac rupees investment for 20 years at 10% annual interest. Can you guess the final amount at the end of 20 years?

25 lacs? 40 lacs? 55 lacs?

Your investment after 20 years would be 67 lacs.

6.7 times your initial investment.

That is a mind-boggling figure, given that you don’t have to do anything.

You can check out the article on the power of compounding for more in-depth knowledge.

That is a mind-boggling figure, given that you don’t have to do anything.

You can check out the article on the power of compounding for more in-depth knowledge.

Let’s understand the importance of time with another story:

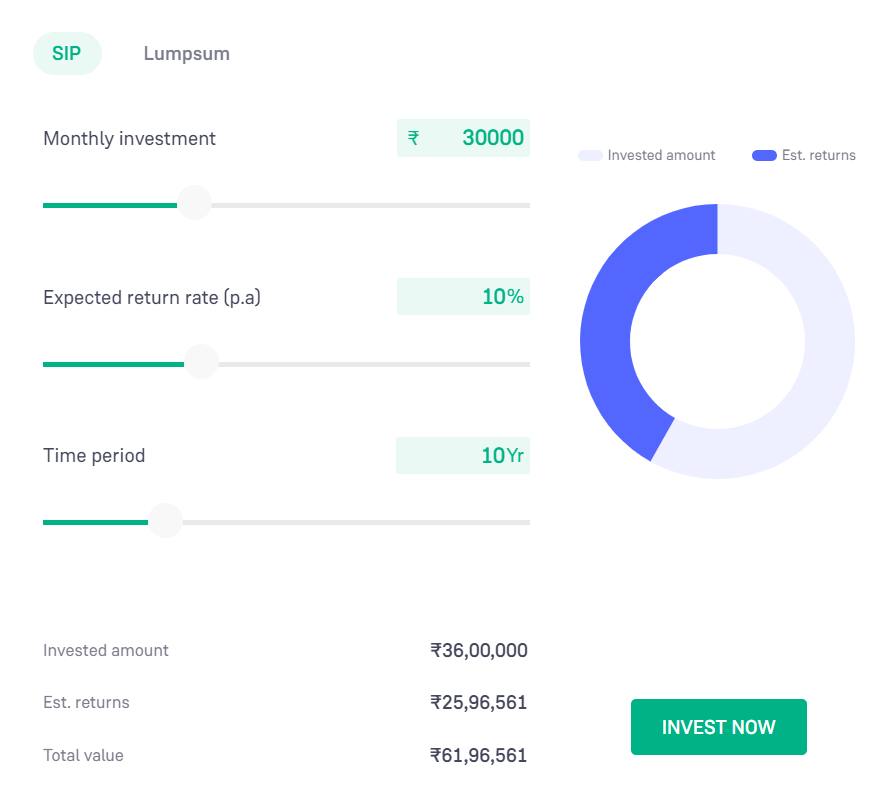

You and your friend earn 70K rupees, both aged 20.

Let’s say you decide to invest 30k every month till you are 30, but your friend chooses to enjoy his life and take a break from investing.

Since this is a type of SIP investing, let’s see how much you save at the end of the decade.

At the end of the decade, you would have made approx 62 lacs.

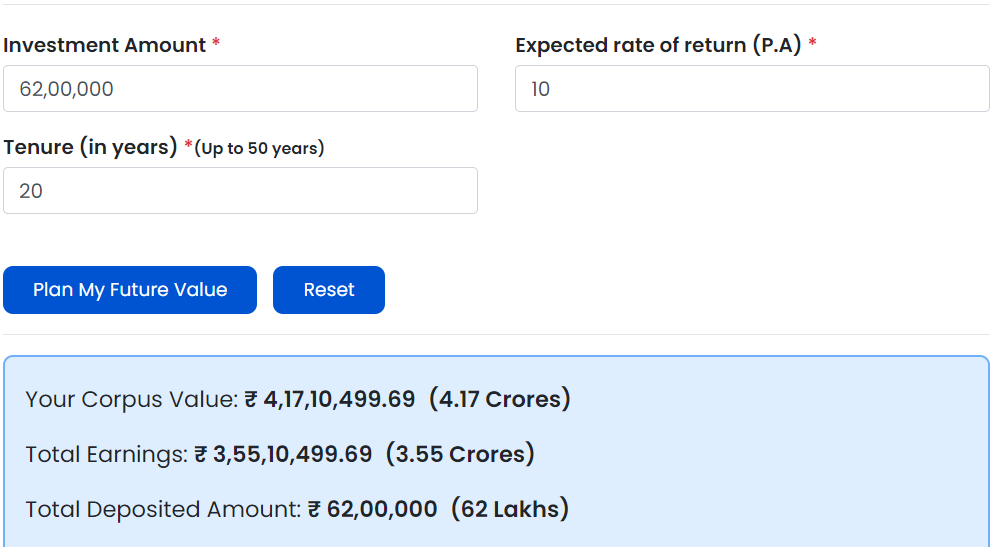

Now, at age 30, you still don’t want to touch this investment. You have your salary and other earning sources. So you wish to leave it for another 20 years and use it at age 50, maybe for buying a house or any other event. But alongside this, you decide not to put up any more money.

So you have only invested for 10- years with a total of 36lacs.

When you turn 50, your investment at 10% interest will have grown to 4.17 Crores.

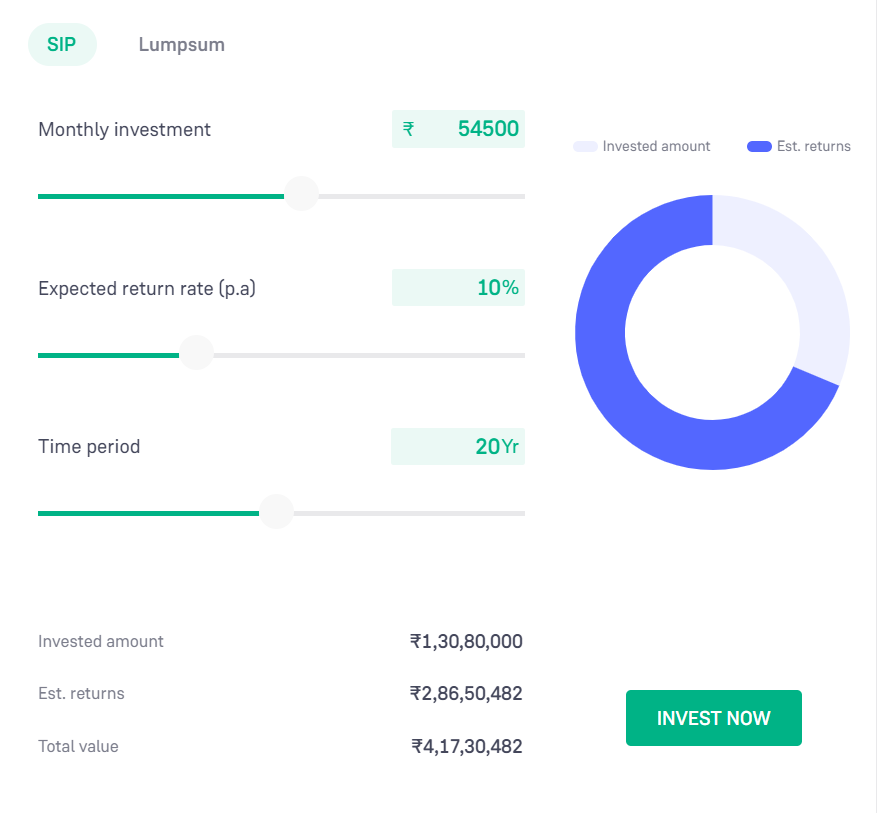

But remember, you had a friend who did not invest till 30. But now he wants to invest, and he plans to invest for a much more extended period. He will fund for 20 years( 10 more than you) and also want to reach the same corpus level as you when you both are 50 years old.

Can you imagine the monthly investment he needs to make for 20 years to touch 4.17 crores?

He would have to invest about 54,500 rupees every month for 20 years or 240 months straight to reach the same level as you.

And, also note the total amount invested to reach this point.

It’s a staggering 1.3 crores.

Just by investing 10- years prior, you not only saved about 95 lacs, but also your finances would be much more relaxed in the later years. You would not have to set aside any money after 30 till 50. You could have used it to do more adventurous and exciting things, but your friend had to set aside a large portion of his income for investment and live on a tight budget. That’s the value of investing early.

Allocation of funds:

How should you invest your money? How much money can you keep aside for a safe investment plan? Does being willing to invest more compromise your living standards? These are some crucial questions cropping up every time one thinks about investment.

The most common advice is the 50-30-20 rule.

In reality, the rule is straightforward. You are required to divide your in-hand money into three equal portions. 30% of income is spent on wants, 50% on needs, and 20% on savings and investments.

You can have separate bank accounts for this feature, and you will easily program yourself for good savings.

By doing this, you will have established buckets for everything and be operating inside each bucket’s allowable limits. It will help you develop discipline while ensuring that you don’t sacrifice the standard of living or your long-term planning. Let’s examine how to divide your spending into three categories—needs, wants, and savings.

Needs are the things you need to survive or must accomplish to survive. Needs are commitments you must meet to live happily, such as getting groceries and food, paying rent or a mortgage, paying insurance premiums, making the minimum debt payments, and more.

Breaking the 50-30-20 Proportion:

Needs: 50%

This rule states that you can utilize half of your after-tax income to pay for things constantly on your list of essential expenses. If you don’t make these payments, you’ll get into problems or accrue debt for the next month.

Luxuries like cable TV, a Netflix subscription, a gym membership, parties, etc., are not listed in the needs section. The 50-30-20 rule states that you must eliminate some items from your “Wants” list if you spend more than 50% of your after-tax income on necessities. If that isn’t an option, your only choice is to downsize your lifestyle and rely solely on what is necessary and required. A minimalist lifestyle could be the solution to all of your issues with lifestyle inflation and spending excesses.

Wants: 30%

“Wants” are the luxuries money can purchase, as the word suggests. These are aspirational goals rather than necessities for fundamental survival. It is also the most difficult portion to explore since, unless you’re a modern-day Buddha who is content with the minimum necessities, your wants are limitless. Wants are items you enjoy having, such as occasional dining out, movie dates, leisure trips, seasonal shopping, splurging on grooming products, hobby classes, etc. As you can see, the list of “wants” is never-ending and, if left unchecked, can consume one’s savings.

Join our Mailing list!

Get all latest news and updates.

Savings: 20%

The savings account is what will get you through the future, while necessities and wants take care of your well-being in the here and now. Perhaps the most crucial bucket is the one that receives the least attention.

According to the 50-30-20 rule, 20% of your post-tax income needs to be saved and put to use through investments. Please keep in mind that in contrast to requirements and wants, saving should always be a top priority.

If you can lower your expenses or your income is too big that only a small portion is for daily expenses, it is an even better situation. You can invest more money and live a relaxed life easily.

Distribution of your savings:

Now you have decided how much money you can fund. The next stage comes about how to invest this money. What are the assets used to invest your money?

There is only one kind of instrument I would talk about in this article, which I believe is the best avenue for any working-class individual.

The Mutual Funds

A mutual fund is an assortment of funds that a fund manager professionally manages. A trust that pools money from numerous individuals with comparable investing objectives and then invests it in stocks, bonds, money market instruments, or other securities.

There are different kinds of mutual funds depending on your requirements. You can open any platform like Groww or Paytm Money and learn about various funds.

Our focus is mainly on two kinds of mutual funds:

- Index Funds

- Debt Mutual Funds

Index Funds

This fund follows the index of any market like Nifty, Sensex, S&P500, and many more. By investing in index funds, you invest in all the index companies and wait for the money to grow.

On average, the average returns of an index in India is around 11-13% annually, This kind of return stretched over a long period is more than sufficient for a working-class person.

I have written a detailed article here. You are encouraged to read more about the index fund in this article.

Debt Funds

A debt fund is a Mutual Fund scheme that invests in fixed-income instruments, such as Corporate and Government Bonds and corporate debt securities that offer capital appreciation.

Our ideal distribution of funds between the two would be 80% equity and 20% debt.

This 80:20 distribution is on the foundation of meeting long-term and short-term needs.

Any short-term need (within 3-5 years) should be met with debt funds. These funds allow you to grow your money and be there when you need it. Whereas, the index funds are for long-term requirements, maybe buying a house, any big event, and even retirement. You have to give a while for the index funds to provide the kind of return you are hoping for.

And you know by reading the story above, when given enough time the power of compounding can do wonders for you and your future.

One thing to note is that the 80:20 rule is just a point of reference. You would need to bend these numbers to satisfy your future needs. Just remember that the distribution should be such that the short-term needs get fulfilled by your debt funds only. Never touch your equities to meet any near-term expenses.

Conclusion:

The early investor always has the last laugh. Be disciplined and make regular investments to ensure a safe and relaxed future. Also, if you find any person who is beginning their investment journey or thinking about it, encourage them to learn and find out more about their finances and help them map their future.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.