Skip to content

Skip to content

7 Bad Money Habits and How To Break Them

Money is an integral part of everybody’s life. It lets you get things. You can fulfill your needs and wishes when you have the money. Money bridges the gaps between your dreams and your reality. It is one of the most powerful tools ever create. But as the saying goes, “With great power comes greater responsibility.” If you are unaware of your spending habits, this tool can quickly spiral into crises, trapping you forever.

In this article, you will find the 7- prominent Bad Money habits and how we can break these habits.

7 Bad Money Habits

Bad Money Habit #1: Buying Things On Easy Monthly Installments or Loan

Buying things on The Easy Monthly Installments might seem like an easy and pocket-friendly thing to go for, but this is one of the biggest mistakes that can impact your savings in the long term.

Unless you buy a house or going to spend money for education, having to take on an EMI, or even a loan for that matter, is a serious no.

I have seen people take out loans to have a big grand wedding that takes place for a day or two and pay it back for 10-20 years.

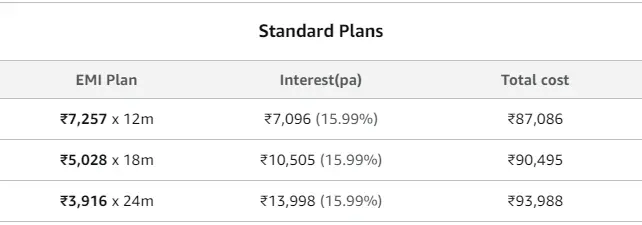

The interest rate on loans or EMI plans ranges between 16-48% annually.

No instrument on Earth can grow your money at that rate.

Your savings and growth generally range between 8-10%. When you can not earn or grow your money at that rate, why do you need to create an expense that sucks up that much money from you?

When you buy things from Amazon on easy EMI, go out on vacation, and transfer expenses on the credit card, which you then convert to EMI, all lead to so much extra money out of your pocket.

Let’s say you want to buy a car for Rs 8 Lac and in this range, you get the basic models of the cars with not so much extra facilities.

Let’s assume that your after-tax salary is Rs 1 lac.

Now if you buy the car on EMI at an 8.5% interest rate, your monthly EMI comes to around 16.4K; not so bad for a person having 1 lac each month.

But for this facility, you pay 1.84 lacs as extra interest over 5- years.

That is around two months of your salary. 2 months of your time is spent working for the bank and not for yourself.

Instead, if you had proper planning and started saving money around two years back, saving 25K a month for 2- years would let you save 6- lacs rupees, and the remaining you can manage easily.

Timely planning would have saved you a significant amount of money and time.

Solution: Before making any big purchase, like any electronic item or other expense, lay out a plan as early as possible. Rarely will you fall into such a situation where you have to cough up so much money immediately.

You could even create a separate bank account so you don’t use it before achieving the target. You can reuse it for your next target. It could be a vacation, a new smartphone, or maybe your house if you want to buy it in cash.

Bad Money Habit #2: Overdrawing Your Credit Card

Credit card is a two-edged sword. If you do not use it carefully, you might land in trouble. Generally, banks provide a credit limit to their cardholder based on the candidate’s profile, earnings, and tendency to pay back the money.

If you are maxing out your credit card regularly, even though you pay it back timely, you need to be careful. If you miss your deadline even by a single day, a lot of interest and penalties are coming along your way.

Some of you might even consider overdrawing the credit limit in the expectation of paying it back the next month. Firstly, when stretching your credit card beyond the limit, you are slapped with a fixed fee for this facility. And on top of that, you pay additional charges on the amount withdrawn.

Do you see the problem here?

There are charges after charges, all designed to take up more money. Finding yourself in such a position is not a good thing.

Solution: The first step you have to take is to go all cash and find employment with better earnings. It is the core step you would have to take. Pay back all the dues that you currently hold. It might mean living below the means, but it’s all worth it when you pull yourself out of the debt trap. Start building an emergency fund for yourself so you do not fall into any such situation again.

This one is optional, but if you are successful in the above step, try to have one or two extra credit cards from different banks and split the overall expense. It will not only improve your credit score but also reduce the chances of you forgetting about making the payment.

Bad Money Habit #3: Not Having Health Insurance

It is a no-brainer, yet many people do not have health insurance. In India, only 37% of the population is under medical insurance. Hospital care expenses are increasing significantly and will cost you a fortune if you ever undergo any major surgery. If you do not have sufficient funds, you fall into a debt trap, making it very difficult for you. To prevent such things from happening, it is of utmost necessity to have health insurance from the leading providers. These insurance agencies pay your hospital against your medical bill so that you can focus on recovery.

Solution: Check out the article on how to choose good medical insurance according to your needs.

Bad Money Habit #4: Spending On Cigarette/Liquor

Another habit impacting your money management is the expenses on cigarettes and alcohol.

Taking the data set from this article, you can understand that a person spends around 25 lacs in his lifetime if he smokes five cigarettes a day.

If you add the cost of alcohol, the figures shoot up much more.

Not only do these substances affect your purse, but affect your health and sometimes have led to many serious accidents and other problems.

Solution: It is such an addicting habit that you can easily find yourself in a vicious cycle. Make sure to stay away from it as much as you can before it becomes an addiction.

It might mean disconnecting with peers involved in drinking and smoking. You may have to make many tough choices, but it will ensure your safety and sanity.

Bad Money Habit #5: Making Impulsive Purchases

The father of all culprits. Online shopping has increased so much that people find it difficult not to buy things on sale. These giant companies spend millions of dollars making eye-catching advertisements and marketing campaigns that tempt you to buy stuff you don’t want.

If this continues for the long term, you are bound to make purchases beyond your income, leading to maxing out your credit cards or buying things on EMI.

Solution: First thing to do is to uninstall all the e-commerce-based apps on your phone. These apps keep sending regular push notifications to entice customers. If you have upcoming shopping needs that cost you substantially, postpone it for 7-10 days. Many times, buying the product is just a temptation. But even after 7-10 days, you still feel the need to buy, analyze whether you need it, or you can use an alternative. Delaying gratification can reduce your unwanted expense by a significant amount.

And you can even use the platform Honey to reduce your final bill.

Bad Money Habit #6: Revolving Credit Card Debt

The credit card you hold charges you anywhere between 36-48% for the interest rates when you have any amount pending.

Credit cards are a great tool to make your life easier, but make your life a living hell if you are not careful. Avoid spending more than the decided expenses each month, and do not make any unplanned expenses.

Solution: Make a monthly budget for your possible expenses for the future and stick to it. Do give yourself some room to wiggle but not so much.

Build yourself an emergency fund, and when the need arises for the emergency, use it. You will not have a credit card loan over your head and can build up for the lost capital.

Bad Money Habit #7: Increasing Your Standard Of Living

When you get suddenly filled with cash in your bank account, you get bound to fall victim to your temptation. It happens to everyone, but there should be a limit to it.

Many people I’ve seen who could survive on a 50K monthly wage are now finding it hard to manage their expenses with a 1.5 lacs salary. A bigger salary can easily give you a credit card with a better credit limit. Once you get a credit card with no control over your behavior, you are bound to make unnecessary expenses. It is because of those temptations. You think you need all those things, whereas, in reality, you are safer without them.

Solution: Pursue delayed gratification. Buy things with some delay so that you are fully aware that you need something or not.

One trick is to invest the money as soon as it hits your bank account. Set aside some money( make sure it is at least 50% of your salary) for actual expenses alongside some fun money, but apart from that, invest everything into any instrument of your choice. It might need some effort beforehand, but it is a one-time cost and can reduce future upsets significantly.

Also, disconnect any credit card service if you think you cannot control the spending. Go all cash. There is no problem with it if it helps you manage your goals.

Check out the Financial Education series for a series of articles to make better money decisions.

Conclusion:

Like any habit, you must refrain from practicing bad financial habits consciously for a while till they become a way of life for you. These habits will help prevent losses in your personal finances and secure your future.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.