Skip to content

Skip to content

Don't Leave Your Future To Chances: Understanding the Importance of Medical and Term Insurance

In this article, you will learn about the importance of Medical and Term Insurance which is the next stage of building an empire of financial freedom.

Today’s article focuses on one of the least thought-about financial products, yet this product is so crucial. Without these products, you could go many years back on the journey to financial freedom. These two financial instruments are:

1) Health Insurance

2) Term Insurance

If you look at a detailed analysis of medical insurance in India, you will see that many people have still not understood the importance of health insurance and how it can protect them.

We will talk about each separately, but before that, let’s get to our POT STORY first.

When you intended to shift from one place to another, you did one specific task toward your POT.

You added a protective layer around the container and kept it in a case due to two reasons:

i) If the Pot breaks and you lose all your water, it would be difficult for you to provide the necessary things to your family and impact your journey of passing the country according to your plan. Thus protecting yourself from this unfortunate incident is very much required.

ii) If the Pot breaks, you not only suffer from the lack of necessary water, but you would have to spend time again looking for more water in unknown terrains where it is not even sure if you’ll find any. Thus it increases the risk exposure.

Ideas Behind It

These two reasons revolve around two different ideas:

a) The first reason revolves around the mitigation of loss. Nobody expects to face a loss or be at the receiving end of sad news. So to reduce the chances of such an event, covering up the jar was necessary.

b) The second one is based on the correct utilization of time. Time is the only thing that is constant for every person. Making the highest and the most productive use of your time is always the intent. So when you expect results from your work, the next logical step is to conserve it to the best of your ability so that you do not have to do it again, leading to lower productivity.

These two factors also govern our life; that is where health and term insurances come into play.

Health Insurance

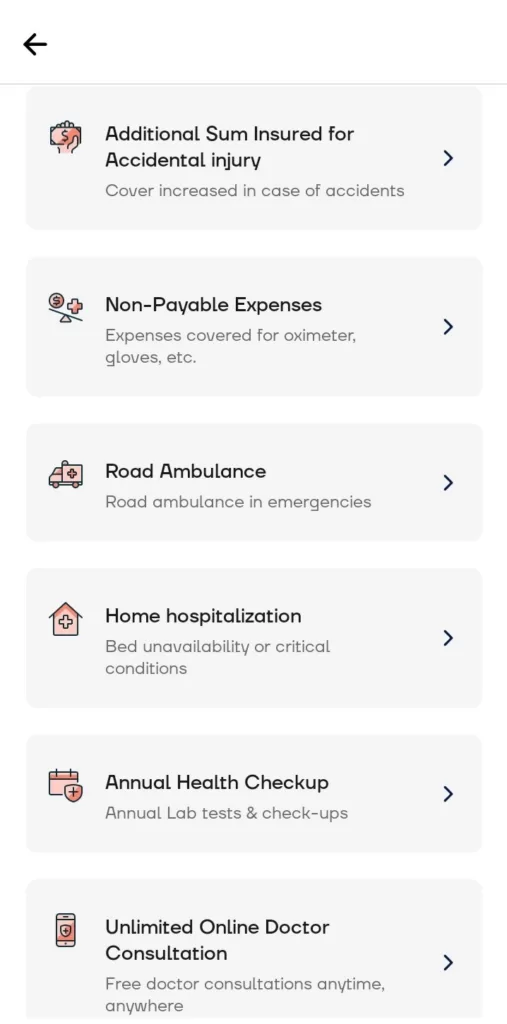

Health insurances play a crucial role when you end up in a hospital bed due to any reason, and the expenses are to be paid by the insurance companies.

With a small fee which is the insurance premium, you can save yourself from many financial disasters.

Everyone is aware of hospital expenses these days. You must have heard of many instances where someone’s monthly salary gets consumed due to a single-day hospital expense. Such has become the hospitalization rates.

So if you do not have any insurance and go about your life as if you will never get sick and save all your money, you never know when a single event can use up all the money, and you might end up with nothing.

All your dreams of lavish homes, vacations, and all plans go down the drain.

Such has been the importance of medical insurance that even the government provides a tax break for those who buy medical cover for themselves and their family members.

My whole study is on the Indian Insurance Market, so if you encounter any foreign term, search it on the internet concerning the Indian market only.

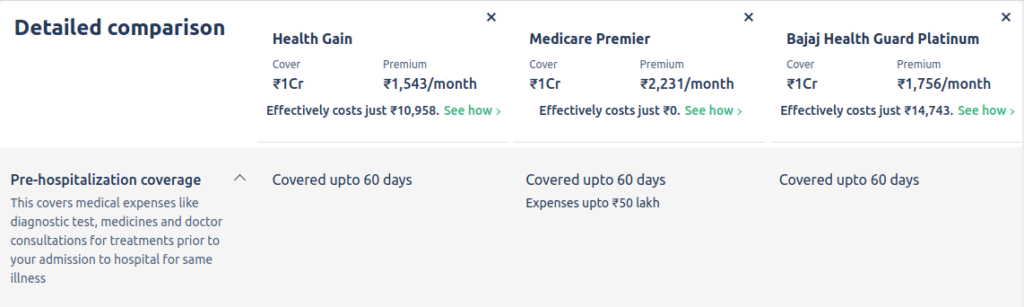

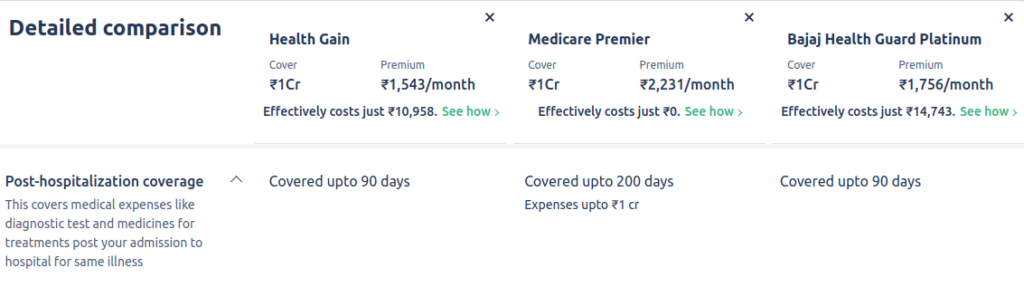

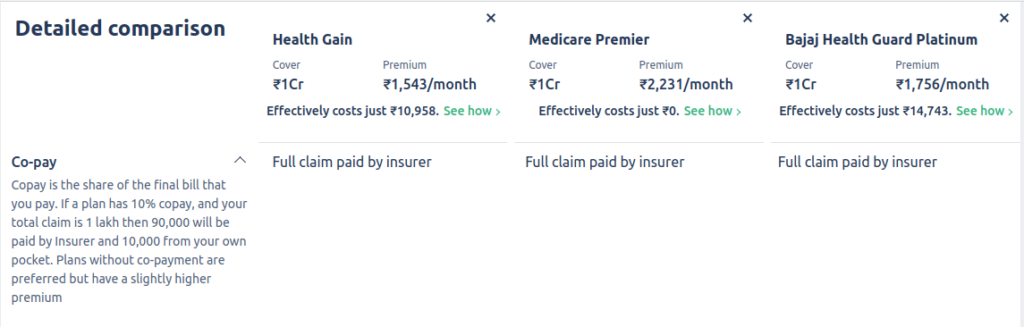

For explaining the parameters, I have taken 3 insurance providers and we will compare them on each of these parameters.

Do note that these insurers are not at all any form of recommendations. These providers are established companies with large audiences so it could be easily used for education purpose. Do your own due diligence before choosing any insurance provider.

These companies are the Reliance, Tata and Bajaj.

The following prices and cover are for a 24 year old Male.

1) Coverage

The first question you should ask is regarding the coverage amount. How much insurance coverage do you require?

On average, a cover between 5-15 lacs per person should be sufficient for you. But, if you are among those who face frequent medical problems, you should go for broader coverage.

Moreover, the cost of hospitalization in metropolitian cities are much expensive.

Then in the coverage, you have the option of a family floater where your whole family gets insured for a large sum, and anybody of the insured members can use the funds.

First, understand your needs and then decide about choosing any of the above options.

Join our Mailing list!

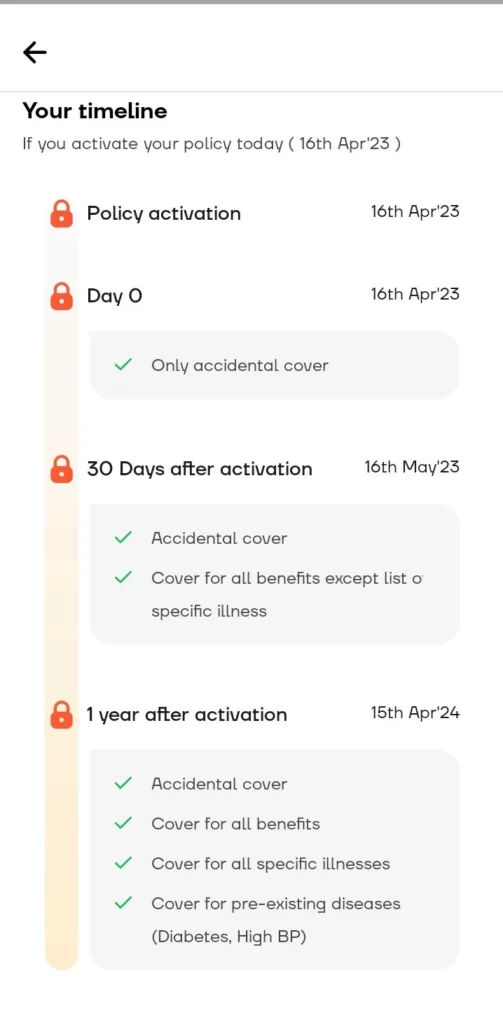

2) Waiting Period:

Whenever you purchase medical insurance, the first 30 days are the waiting period for your plan. During this duration, you cannot claim any benefits unless it is due to an accident.

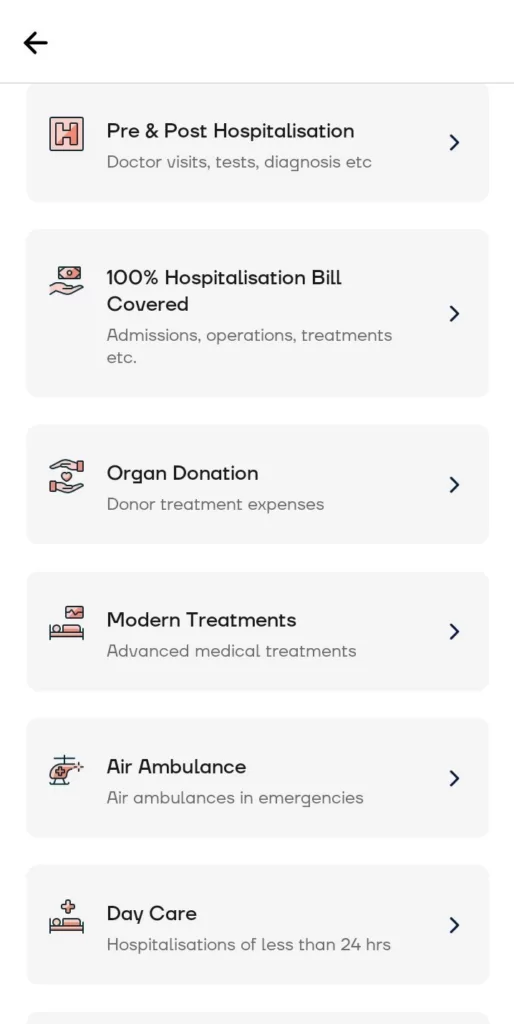

3) Pre and Post-Hospitalization:

Your insurance plan must explicitly specify the kind of service they offer before and after a scheduled surgery. Learn about these benefits and compare them with different insurance providers.

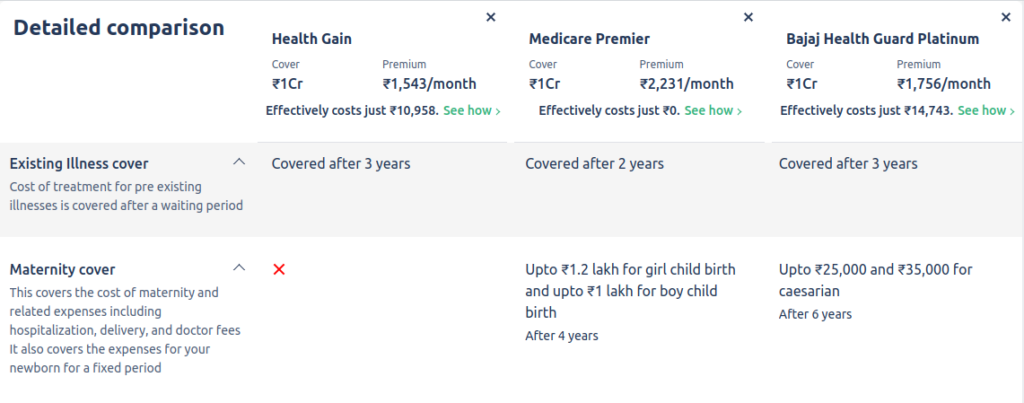

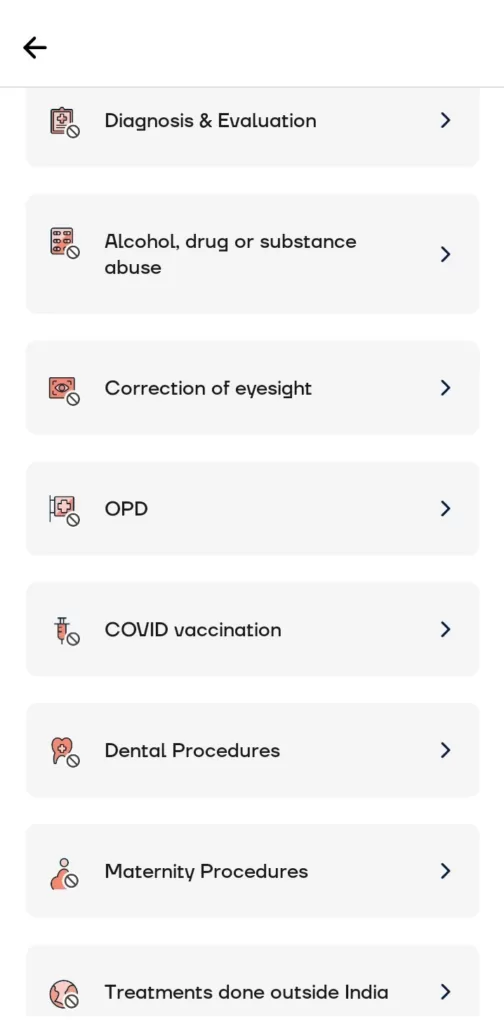

4) Pre-existing Diseases:

If you get detected with any ailment and then intend to buy medical insurance to pass on the expense to the agency, this will not work as many of these agencies have either 24 months or 48 months waiting period to provide you the medical coverage of any pre-existing diseases.

These companies sometimes may also reject the claims of any issue arising due to these ailments, so make sure to have a correct timeline in front of you about the conditions which do not get covered under pre-existing diseases.

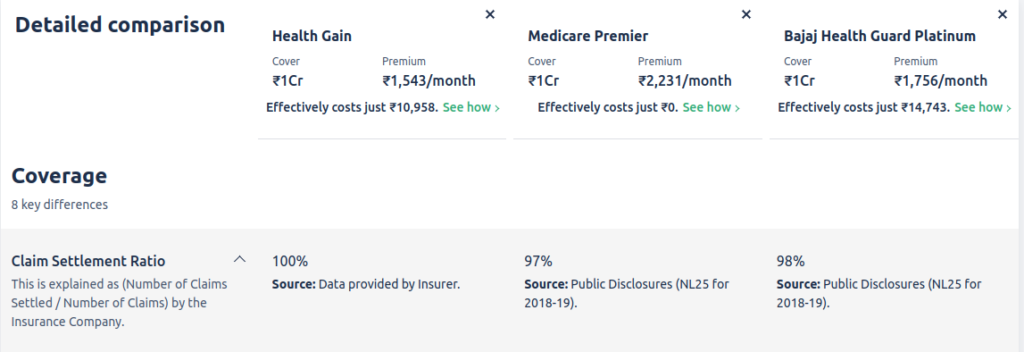

5) Claim Settlement Ratio:

This number tells you the number of claims approved out of every 100 claims made. These agencies are legally required to publish the numbers regularly and thus give a better opportunity for the user to make an informed decision.

You should not pick any agency with a score of less than 96. The higher the number, the more the claims are approved. The better for the patient.

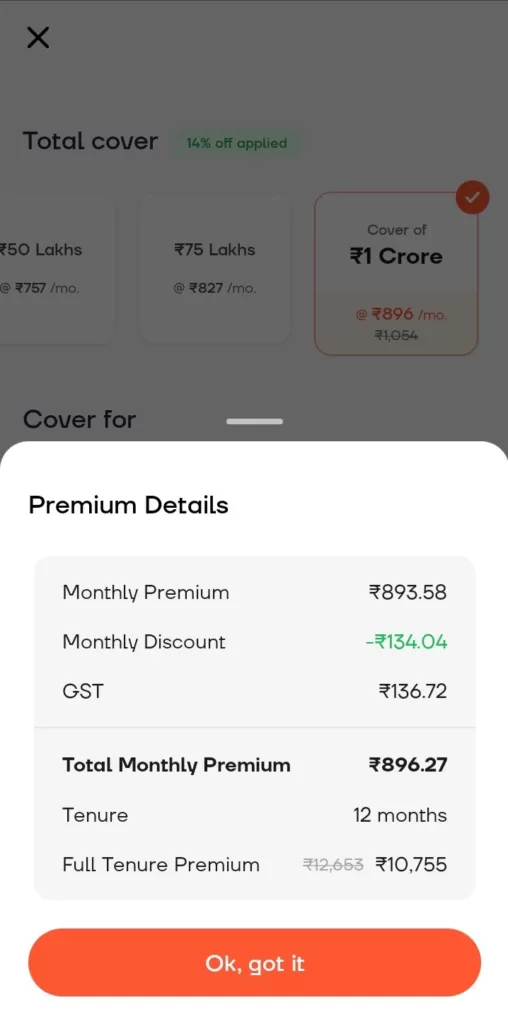

6) Pricing:

Check out the pricing of the policies with a gap of 10 and 20 years. You want to know how the prices change as you age. Any cheap medical insurance could become very costly in later years, and then you would not have the option to switch as very few agencies are willing to insure older people.

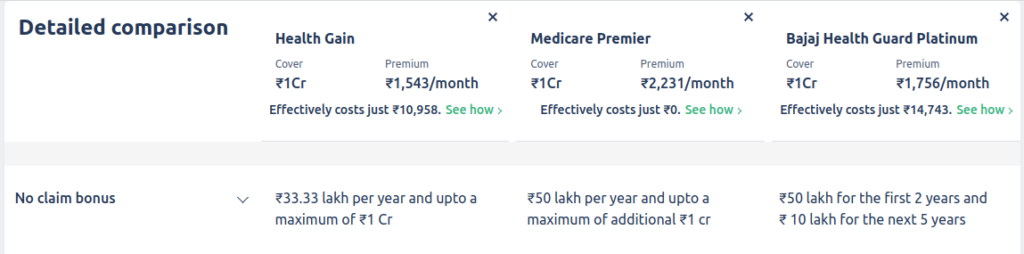

7) No-claim bonus:

When you do not make any claim for a year, the agency provides you with a no-claim bonus., which is 5% of your plan. The bonus gets added to your coverage, and the premium is usually the same.

8) Exclusions:

Some surgeries and procedures get excluded from medical policies. These include cosmetic surgery and any cancer-related ailments unless you have a cover for that. You must read the list of these procedures and determine which company offers you the best services.

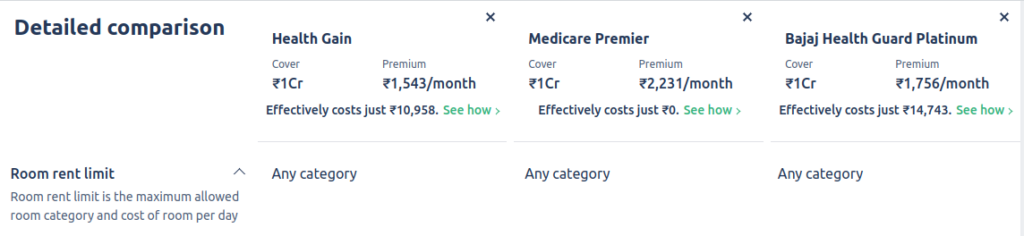

9) Sub-limits:

Many insurance companies provide a limit on certain things specifying the maximum amount the companies will pay. It usually includes the room rent. Room rent can vary depending from region to region, so the company uses such a clause to prevent unwanted expenses.

10) Co-Pay:

The final element for you to look at is the co-pay clause. This clause says that the patient will pay a certain amount of the hospital bill, usually around 5-10%. Look for this clause and decide on the one with a zero co-pay clause or minimum co-pay.

Make sure to understand each of the parameters and find the suitable plan for you and your family.

The above images are derived from the insurance provider named PolicyBazaar. You can even check out their website to consult with them.

Apart from these companies, there is another insurance provider which has built up good reputation.

It is Navi Health Insurance. I am attaching the services provided by them under the same parameters. Make sure to check them out for better comparison.

Navi Health Insurance

Services Offered

Term Insurance

The next step to shield yourself and your family from financial disaster is to buy a term insurance plan.

Term insurance is another important financial instrument that many people ignore.

In term insurance, you pay a premium against insurance where the condition is your family will get a large corpus in case of your death when the insurance is active but won’t get any money back if you live through the insurance period.

Whattttt???? Won’t get any money back???

Why on earth would I buy such an instrument or a product that does not give me any of my money back?

It is the general Indian mentality that I have come across. And I am not blaming the families for having such thoughts. It is because many have not been able to receive any sound advice on investment strategy or making your financial journey shockproof.

I know you might still be skeptical about term insurance, so let me give you 3-instances:

Join our Mailing list!

Instance A

You work hard, make the regular investment, and all your financial planning is in order. But suddenly, you die. You died in an accident, and now your family is without you. All your savings and investments are relatively recent, and for it to become a rewarding investment, it must take years to compound.

But your family needs to meet expenditures. They can’t survive without money. So they take the harsh step of using up their savings and meet their expenses. Moreover, they can only use the amount which you earned.

All your efforts are down the drain.

Instance B

Consider a similar situation as mentioned above, but this time you had term insurance made for your family. After you die, your family receives a large sum, usually, 20-25x your regular savings. Your savings are still intact and can serve your family in later years. Your family need not worry about finding new income sources and meeting expenses.

Instance C

The third instance is one of the best that you would want to happen. You buy a policy, earn for your family, and regularly invest in sensible opportunities.

You get to age 85, which is generally the upper limit of your insurance. At this point, this is sure that you will not get any money back, but the insurance plan provided a safety net for your family had you died. All your investments would have come to fruition as they had enough years to compound, and you and your family still have a large corpus to serve you.

If I were to give you options to pick the most suitable instances, it would be:

C>B>A

And who wouldn’t like that?

After all, we all are earning money to survive and provide for our families.

But you might argue that isn’t it possible to buy a term insurance plan which pays back the money if we survive.

You are right; there is.

And it exists precisely to fool ordinary people who think that all this personal finance is too tricky and let the so-called experts handle it.

These experts exist to make money for themselves, and when people who buy into such policies become their victims, they get their hefty commission.

I am sure that you will not buy this argument unless you study its maths. And I expect nothing less from you. To not make this writing too long than it already is, I have created a separate article to clear your mathematical doubts.

When To Buy A Term Insurance

The sole purpose of term insurance is to look after your dependents in case of your demise.

So, if you already have some family members you look after, you should buy a term insurance plan if you haven’t bought one yet.

If you are in your 40s, the premium would be expensive, but that is because you were late to make this crucial decision. And because the insurance companies resent insuring older people compared to the young ones.

And did I tell you that whatever your premium is, it remains the same till the end of the plan’s maturity?

Due to this reason, many people buy the plan as soon as they start earning, even if they do not have any dependents yet. But they will have a family, kids to look to, and even parents to support in the future. It is better to lock in the term insurance at an early age and at a cheap rate.

The above said insurance providers are at no cost any recommendations. These are used for educational purpose only. Kindly do your own due dilligence.

Term life insurance covers you for the duration of the contract. While starting that period at a younger age is typically preferable, the exact timing may depend on when you foresee other people dependent on your earnings. The insurance policy’s duration should be as long as your dependents would require your income. For parents, this often lasts until their kids are adults.

Couples who jointly own a home might wish to be protected until they repay the mortgage.

Parents who don’t have a job would also need insurance because, in the event of their passing, their unpaid work (childcare, etc.) could need to be replaced by paid services (like daycare).

Life insurance may be wise even before you have dependents if you have unsecured debt, such as credit card bills or private college loans. For instance, credit card firms demand payment of all outstanding obligations following the holder’s passing.

Features of Term Insurance:

- Low entry age: Term insurance plans offer a lower entry age, and people as young as 18 can buy a term plan.

- Offers Long-term protection: The term plan delivers long-term protection. You can stay covered under a term insurance plan till 99/100 years of age.

- Easy to buy: You can easily buy term plans online in just a few clicks from the comfort of your home.

- Multiple Premium Payment Options: You can select from a wide range of easy premium payment options when buying the most suitable term plan online.

- Protection Against Liabilities: Term insurance allows you to protect your family against remaining financial liabilities and loans.

- Death Benefits in Installments: When buying term life insurance, you can choose how the benefits need to pass on to your family. It could be lump-sump, or you can arrange a monthly payment plan.

Join our Mailing list!

How Much Do YOU Need?

In this section, we will cover how much insurance coverage you require.

If you remember our first article, I asked you to write down the amount you would require to be financially free.

That money included all your future expenses and was made specifically for your needs.

Although your family’s needs would not be similar to yours, many items would overlap. Therefore, it is a good place, to begin with.

This amount would be able to cover all your family’s expenses. But if you have some outstanding debt, such as if you already have a loan or any other crucial outgoing, it is better to add the amount to the previously calculated figure for safety purposes.

Another approach you can look for is to take 10x of your annual income and get an approximate value. The numbers in the two strategies may not differ to a large extent. You have to choose the more realistic value for yourself.

This was the Goal, I talked to you about in my earlier article. My objective is of 7 crores, but if I die, my family might not want a 4.5 crore house but rather a 1.5 crore house. There might be other areas where they would prefer to cut corners.

Doing this can provide you a good approximation of how much they would need after your death and if you are not satisfied with it, add some buffer to it.

Choosing The Right Insurance:

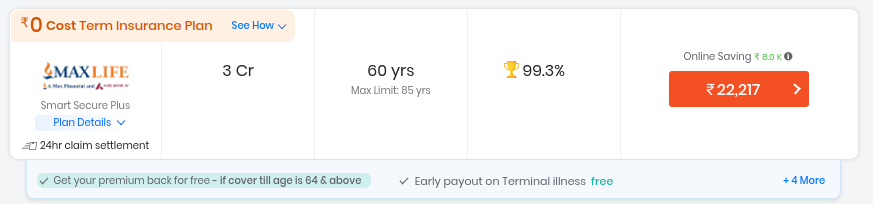

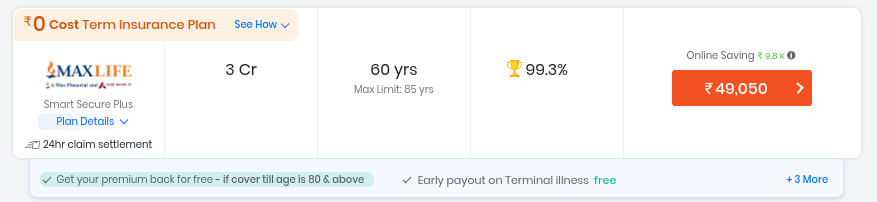

Many reputed companies offer great term insurance, and you will not have that much difficulty finding a suitable plan.

- The first step is to decide the cover amount. You can visit any online platform to buy term insurance or call the helpline for the best advice. You can try PolicyBazaar, check insurance plans on PhonePe or any reputed bank which provides such services.

- The next step is to look for the claim settlement ratio like we saw while purchasing health insurance. Again higher the number, the better for you.

- Check out the pricing of the plans. Choose the one that best suits you.

- Submit the necessary documents required for the purchase of a plan. Some of them are:

- Income Proof

- Address Proof

- Medical Proof

You can get better knowledge about these documents here.

How To File a Term Insurance Plan Claim?

Here is a step-by-step guide on how to file a term life insurance claim online:

Step 1: Intimate the Term Life Insurance Claim You need to inform the insurance company of the policyholder’s death as soon as possible and submit the company’s claims form with the required documents. You can download the claims form online from the company’s website.

What are the Documents Required for Term Life Insurance Claim Process

You can file a life-term insurance claim by submitting the following documents:

- Duly filled term life insurance company’s claims form (available online and offline)

- Medical records like the death/discharge summary, admission note, and test results

- Original term policy documents Post mortem report (if applicable) D

- Death Certificate Photo

- Proof of the Nominee (Voter ID. Adhaar Card, PAN Card)

- Nominee’s canceled cheque, and NEFT mandate form

I know this has been a long article, but it will all be worth it to make you and your family financially secure.

Conclusion

In this article you learnt about the benefits of the insurances and how it can help you provide the support to your damily.

In the subsequent article of this series, we will learn about the importance of investing and a detailed guide to building wealth.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.