Skip to content

Skip to content

Term Insurance Plans with Return of Premium: Are They Worth the Extra Cost?

Term insurance is crucial for good financial stability offering high compensation to the family members in case of the demise of their breadwinner.

If you already have term insurance, I applaud you for your efforts. But if still any of you do not have term insurance underwritten for yourself, you must do that now. I have written an article on how it would be crucial for you and your family, so please take out some time and read it.

Now let’s talk about the decision you will come across while buying term insurance.

When you buy the plan, you will have two options, either pay your premium and get the cover or pay with a clause to receive the money paid after the end of your cover duration.

Term insurance plans with return of premium (TROP) are a popular type of life insurance policy in recent years. TROP policies provide a death benefit to the policyholder’s beneficiaries in the case of their premature death, as well as a refund of premiums paid if they survive the policy’s term. These plans, however, are more expensive than typical term life insurance policies that do not provide a premium refund. In this post, we will investigate if TROP plans are worth the additional cost and assist you in making an informed decision.

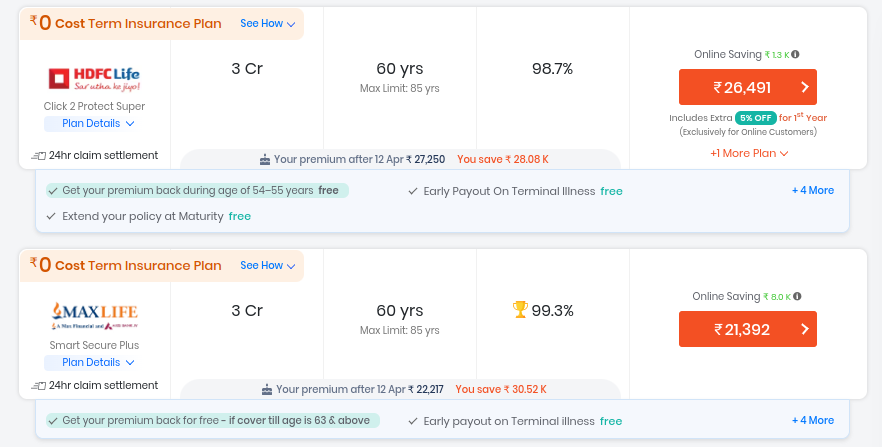

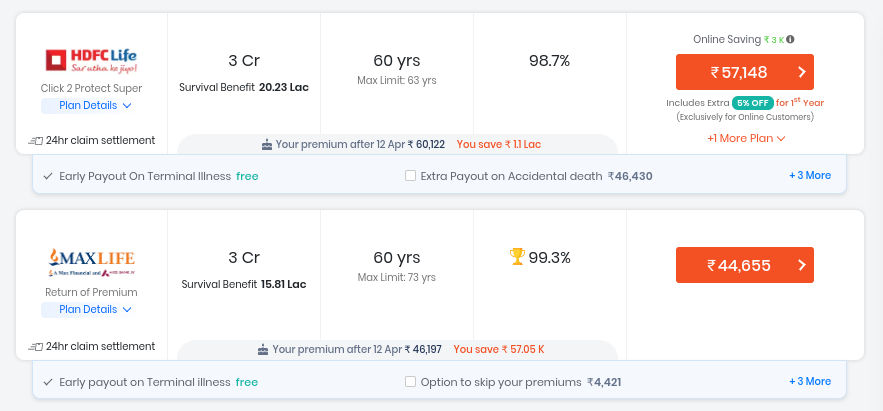

Here are the images of two scenarios.

Both offer the same cover of 3Cr for a 23-year-old individual till age 60.

The one with no return of premium is less expensive than the other.

But you are getting your money under another insurance plan with return of premium.

So isn’t the latter one a better buy even though being expensive?

The human side will pick the more expensive insurance plan one because why not? You are getting your money back. Who wants to lose money, after all?

But does the math adds up?

Let us break that down for you.

For this to make sense, I assue that you are 23 years old and that you’ll live up to 60 years of age.

I am using the number provided for the Max Insurance.

When you choose the first option, you pay 21392 annually for 37 years, equal to 791504.

21392 X 37 = 7,91,504

For the next option, a plan with TROP, your total sum paid after 37 years is 1652235.

44655 X 37 = 16,52,235

You are paying 860,731 extra to get your money back after 37 years.

16,52,235- 7,91,504= 8,60,731

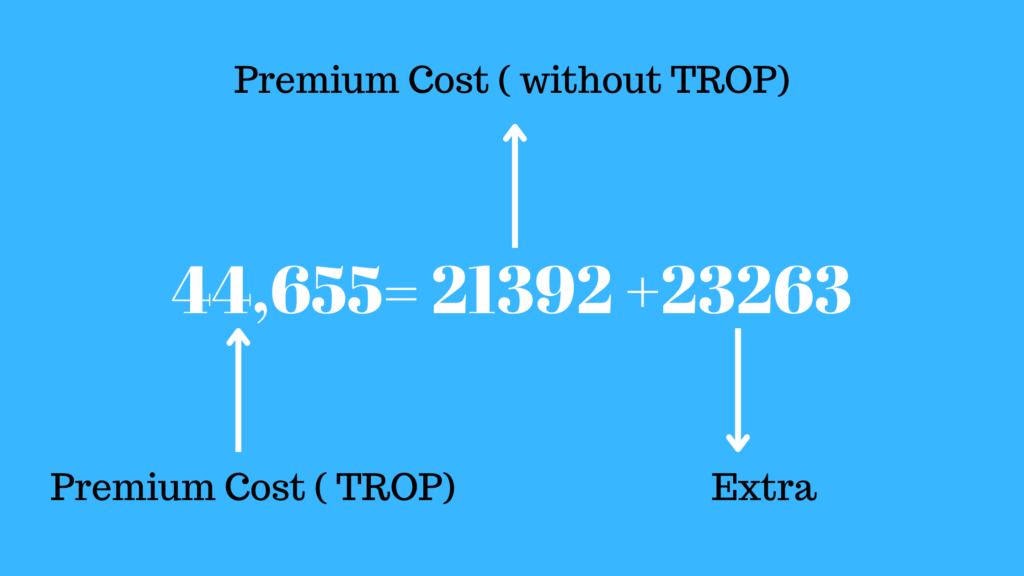

Now, say you break down the 44655 into two segments.

One with the amount of premium where no money gets returned, and the next is the difference.

Now you invest the difference of 23263 into any equity mutual funds for the same duration as your term plan. You are getting the same coverage of 3 Cr, so it is not an issue.

So it goes like this:

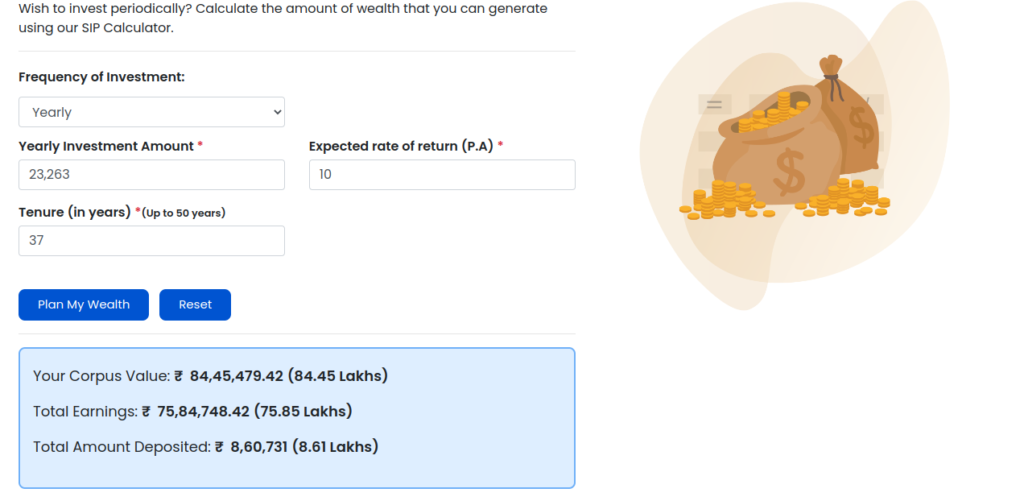

Every year, you pay 21392 as your insurance premium, and 23263 gets invested into equity mutual funds for 37 years.

I am assuming a 10% return rate.

Let’s check the calculator:

You get 84.45 lacs

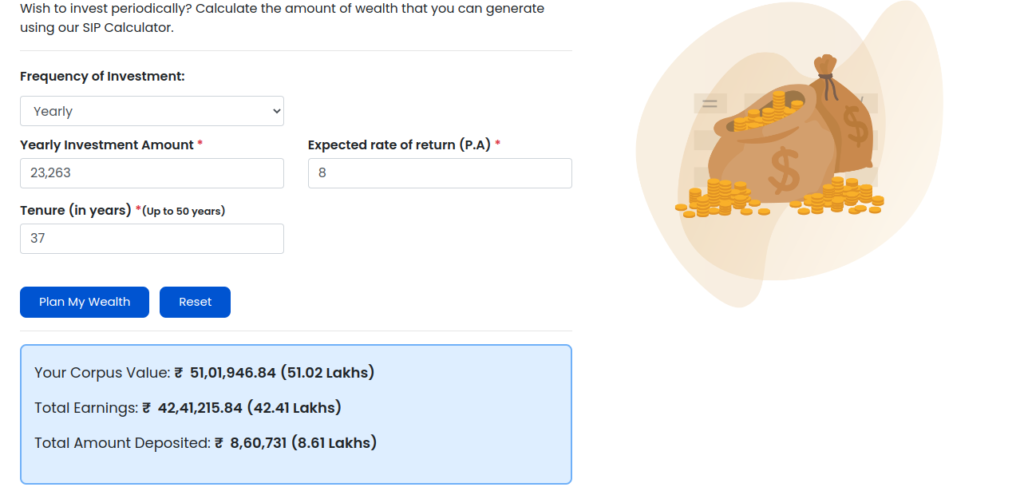

Even if you take a better margin of error and assume an 8% annual growth, the return is 51 lacs plus.

So these are the returns for the extra money you were paying to get back your insurance premium.

For the return of the premium policy, you were paying 8- lacs rupees extra to get your money back of 16.5 lacs.

But instead, if you had divided the money as I mentioned above, you would easily make 3-4x without any added trouble.

Join our Mailing list!

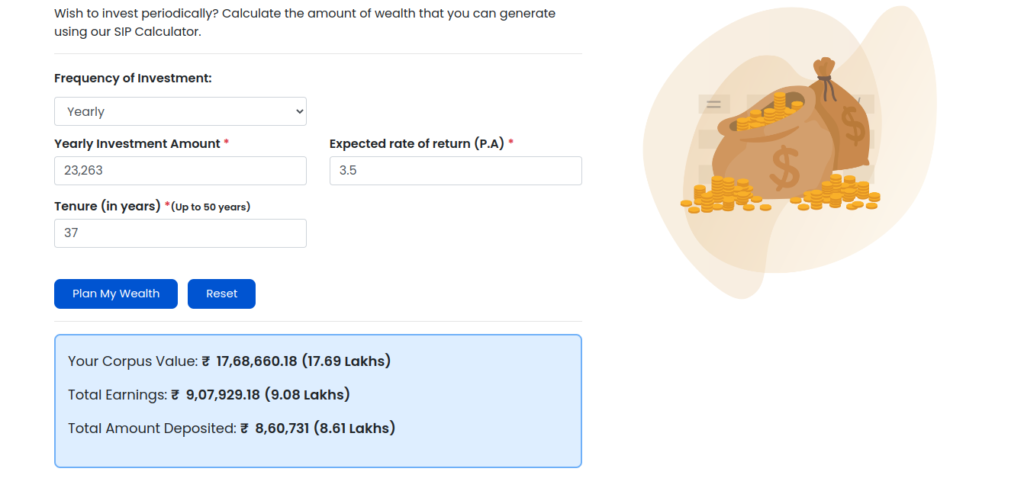

Say, worst comes to worst, and your equity investment grew by only 3.5% for 37 years. If you cannot understand the obvious, for a country like India, this is a very bad return. I highly doubt that we will ever come across to face such a dire situation but let us grow our extra 8lacs rupees with 3.5% for 37 years.

You get 17.68 lacs. Just slightly higher than the sum of the premium paid and the extra amount invested.

So when you think of it, when you divide the money, you will anyhow make your money back. You will at least make 17lacs, the actual amount will be much much greater.

But with a return on premium, you will make a maximum of 17 lacs. It is a very big difference.

I hope this calculation will be enough to help you make a much better decision. The policy sellers try to sell Term Insurance plans with return of premium because they get huge benefits. When people are unaware of their needs, the salesman finds some good way to sell them such dud plans and earn good commissions. They misuse the fear of not investing in equities and use it against them to earn huge rewards.

It is the entire reason I always mention you not to club the purpose of your instruments. They exist for some reason, and anything extra provided to you is just a gimmick and nothing else.

I hope this article was worth your time. If you find it interesting, do share it with your family and prevent them from making such an investment.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.