Skip to content

Skip to content

Investing in Sovereign Gold Bonds: A Diversification Strategy for Your Portfolio

In this article, we will learn about investing in Sovereign Gold Bonds and how it can benefit you to make money.

A lot of people are attached to buying metals such as gold and silver as a method to hedge their investments. Although, many purchase it for personal use, and many use it in times of emergency.

All of this leads to a lot of loss for the investor in various charges. Usually, whenever you purchase a gold bar, you are charged with various fees, such as making charges and taxes.

Moreover, there is always a question about the purity of the metal you buy.

Felt the problems are over?

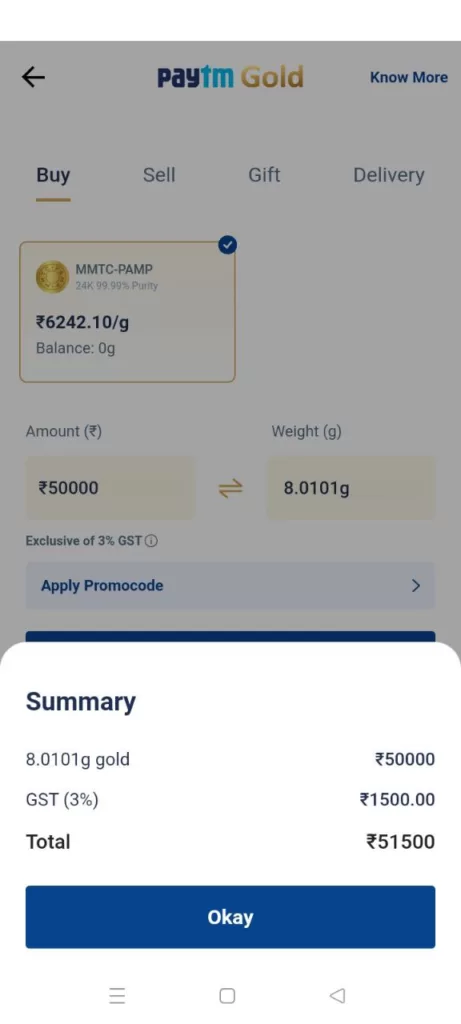

Purchasing physical gold in large quantities is always a tedious job. You not only face an upfront loss of 4-6%. Check on the right hand side. Buying gold online asks you a tax of 3%, physical gold would consume much more of your money. Moreover, after buying, you also have to worry about its protection. If you cannot keep it safe at your house, you will rent a locker and purchase insurance for your items.

Can you see where I am going?

A lot of effort, risk, and charges go into protecting the gold.

Is this all worth it?

In my limited experience, NO!

But there is a way to bypass all of these and reap better profits for yourself.

These instruments are called Sovereign Gold Bonds or SGBs.

Indian investors are increasingly using sovereign gold bonds as part of their portfolio diversification strategies. Government securities called sovereign gold bonds (SGBs) are issued by the Reserve Bank of India (RBI) on behalf of the government and are valued in kilos of gold. They give investors the option to purchase gold without having to hold any of the actual metal themselves.

Benefits of Investing in Sovereign Gold Bonds

Diversion of the Portfolio

Portfolio diversification is a crucial financial tactic to reduce risk. SGB investments can diversify a portfolio and act as a buffer against inflation and market volatility. Gold is regarded as a safe-haven asset and has historically maintained its value throughout periods of economic turbulence.

Interest Income

SGBs additionally provide you with a set interest rate of 2.50% annually, which is paid on the nominal value of the investment semi-annually. You would never find such a service in possessing physical gold. Taxable interest income is received, although resident investors are not subject to tax deducted at source (TDS).

Investment Appreciation

Because of the long-term upward trend in gold’s price, investing in SGBs can also result in capital growth. The investor will profit when selling the SGB if the price of gold increases above the price at which it was purchased. It is crucial to remember that the price of gold might fluctuate and may not constantly rise.

Low Risk

Due to the government of India’s backing, SGBs are thought to be a low-risk investment option. This makes them more secure than other types of gold investments, such as gold ETFs or real gold.

Liquidity

SGBs are quite liquid due to their ability to be exchanged on stock markets. Throughout the stock exchange’s trading hours, investors have the option to buy and sell them whenever they choose. They may also be used as loan collateral.

Cost Efficient

Due to its maturity exemption from the capital gains tax, investing in SGBs is a cost-effective choice. Compared to real gold or gold ETFs, they are therefore a more tax-efficient investment choice.

Tax Benefits of an Sovereign Gold Bonds

Tax Benefits: The primary effect of SGB is the tax advantages that investors receive from doing so, including:

- When you purchase actual gold for more than INR 1 lakh, TDS (Tax Deducted at Source) is imposed at 1%. But, with SGB, there is no TDS charged on the purchase, sale, or transfer, and there is no TDS payable on the interest you get. An investor may purchase up to INR 4 lakhs of SGB.

- Capital gains, which can be long- or short-term, include SGB. You can transfer or sell bonds in LTCG (Long Term Capital Gains) after 5 years; the applicable tax rate is 20% with cess subtracted from the indexation benefits. This updates the purchase price to account for the bond’s impact of inflation, which decreases your capital gains and lowers your income taxability. The 10% tax rate will apply if the indexation advantages are not chosen.

- When you sell or transfer an SGB before three years, the capital gain is known as an STCG (Short Term Capital Gain), which may or may not be relevant.

- LTCG only applies to individual taxpayers; it does not apply to other buyers like HUFs or trusts.

- If you sell the SGB after the lock-in period of 8 years has passed, the entire capital gain (profit on an asset) will be exempt from taxation.

How To Purchase an Sovereign Gold Bonds

At the time of writing, there were no existing issues of SGB. As soon as any issue opens up, we will update this article.

Conclusion:

In summary, investing in SGBs may be a better financial decision than buying physical gold in India due to the fixed interest rate, tax exemption, government backing, liquidity, and portfolio diversification benefits they offer. However, it’s important to consider your own investment goals and risk tolerance before making any investment decisions.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.