Skip to content

Skip to content

Why Guaranteed Investment Plans Aren't as Safe as They Seem: A Mathematical Exposé

Attention: This article is one of the most important articles you will ever come across on this website. After reading this article, if you can understand my views, and even if you do not get much value from any other articles in this series, I will be more than pleased with my efforts.

For many people, safety is frequently a concern about investing. Nobody wants to take the chance of losing their hard-earned money, after all. Guaranteed Investment Plans (GIPs) may look like a desirable choice. They guarantee returns and pledge to safeguard your investment’s capital. Nevertheless, a closer look at the mathematics underlying these strategies indicates that they are not as secure as they appear.

It’s crucial to first know how GIPs operate to understand why they might not be the ideal option for investors. GIPs are usually marketed as safe and secure investment options by insurance companies or other financial institutions. They provide a guaranteed rate of return over a set period, frequently between 5 and 10 years. The investor receives their initial primary investment and the promised returns after the period.

To understand some of the concepts presented in this writing, you have to read two separate articles:

Uncovering The Truth

Recall from one of my previous remarks where I said that you should not combine the purpose of the two instruments of investments. If you invest in any product for insurance, you should get the full advantage of your insurance. On the other hand, if you invest in something for future gains, you should be able to do that efficiently.

Many products market themselves as 2-in-1 product. Be it ULIP plans, endowment plans, or even guaranteed plans. They present themselves as the solution to all our problems. These products vouch to make money for us. On the other hand, ensure they shall look after our family in case of our demise.

But do they?

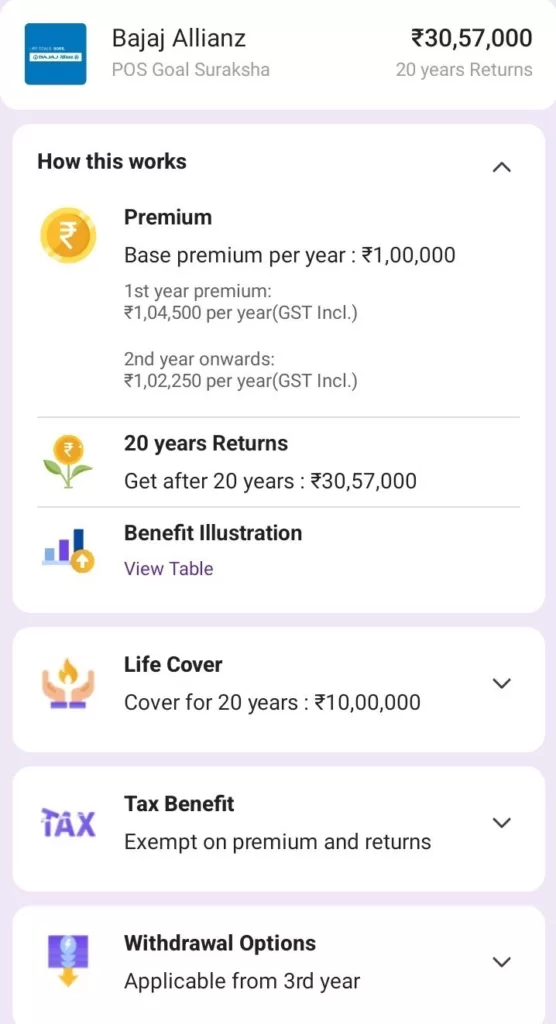

Here is a guaranteed investment plan where you put in 1 lac rupees every year for 12 years and get the following benefit:

a) Life Cover: This amount will get transferred to the nominee in case of your death.

b) Maturity Amount: If you survive till the end of the plan, you will get the final amount.

Join our Mailing list!

Now let’s do some maths:

If you are paying an annual premium of 1 lac rupees, it is safe to say that you will have at least 7-8 lacs as a salary.

If you die during the duration, your nominee will receive 10- lacs rupees.

Now if your home was running on an annual salary of 7-8 lacs and your nominee gets 10- lacs as an insurance benefit, does this make any sense?

The purpose of any insurance is to provide for at least 10x your annual income so that your family does not have to go around and look for new income sources. The bulk amount could help reduce any outstanding debt and maintain the financial integrity of your family.

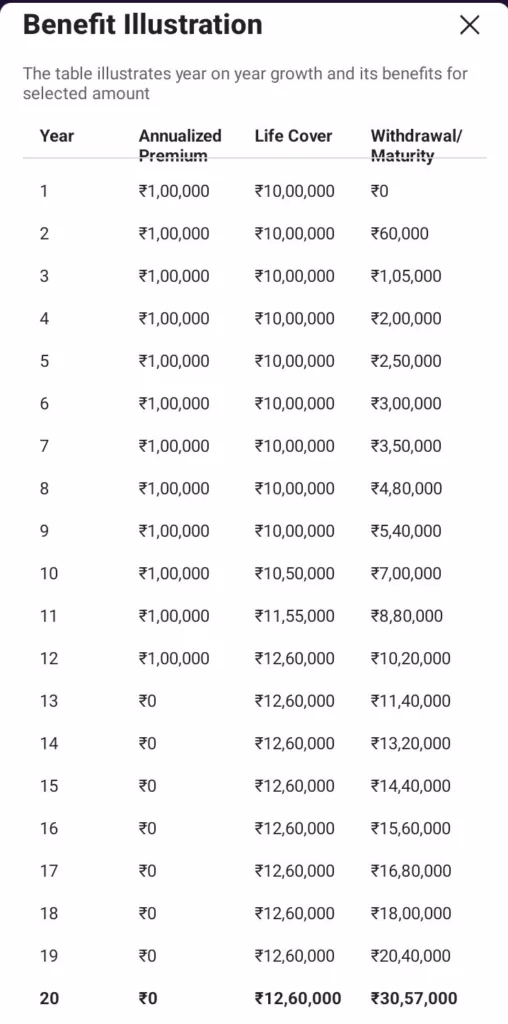

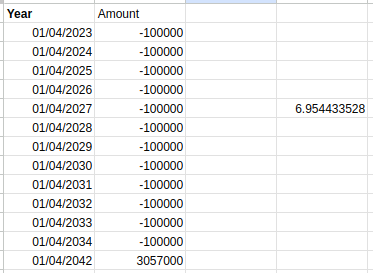

Now comes the second part, let’s say you survive the whole duration and at the end enjoy the 30-lacs as you wished for.

Let’s find the xirr of this plan. If you remember from our detailed article on XIRR, this function provides you with the annual growth rate with which the money has grown.

Step 1: Write down the amount and the dates as shown here.

Remember: The outflows are indicated as negative numbers and the inflow as positive.

Step 2: Use the XIRR function and check the return rate.

The rate comes out to be: 6.95%

If you find this rate of interest attractive, then it might be a good product for you. But remember, the current FD rate of interest is higher than this, and this is the average inflation rate of India. Your money will be eaten up by inflation, and in the future, your money will be valued less.

But on the side not, let us find out what if we keep our investments separate and buy 2- products instead of 1.

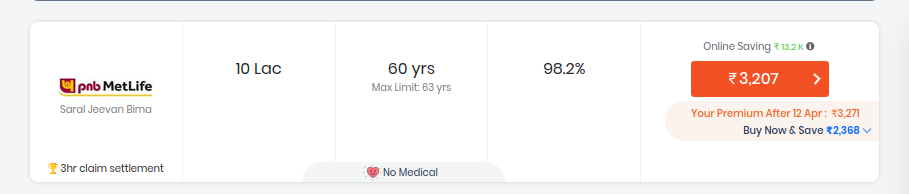

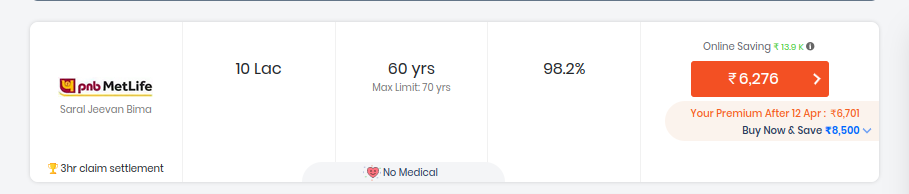

For the same 10- lacs of insurance, the premium you can pay for a 23-year-old is 3207/- but even for a 40-year-old, it would be 6276.

For our sake, take the premium to be 5000.

It means that out of 1 lacs rupees, only 5% is going towards insurance.

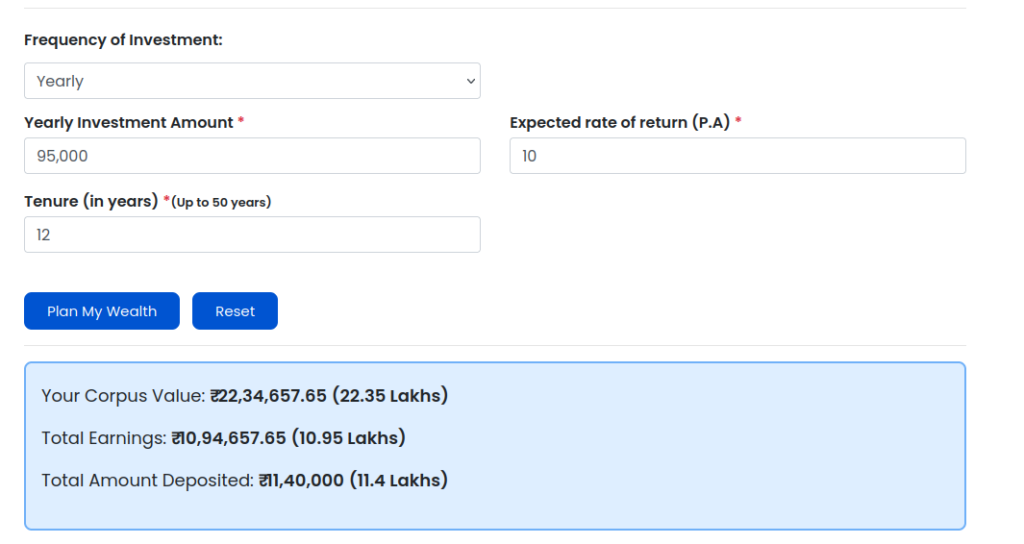

Let’s invest the other 95000 for 12 years into an index plan. The rate for index return ranges from 11-13%, but to have some margin of safety, consider it 10%.

Enter the detail in any SIP calculator, and you will get a value of 22.35 lacs.

But remember, you still have 8- more years left to have your money.

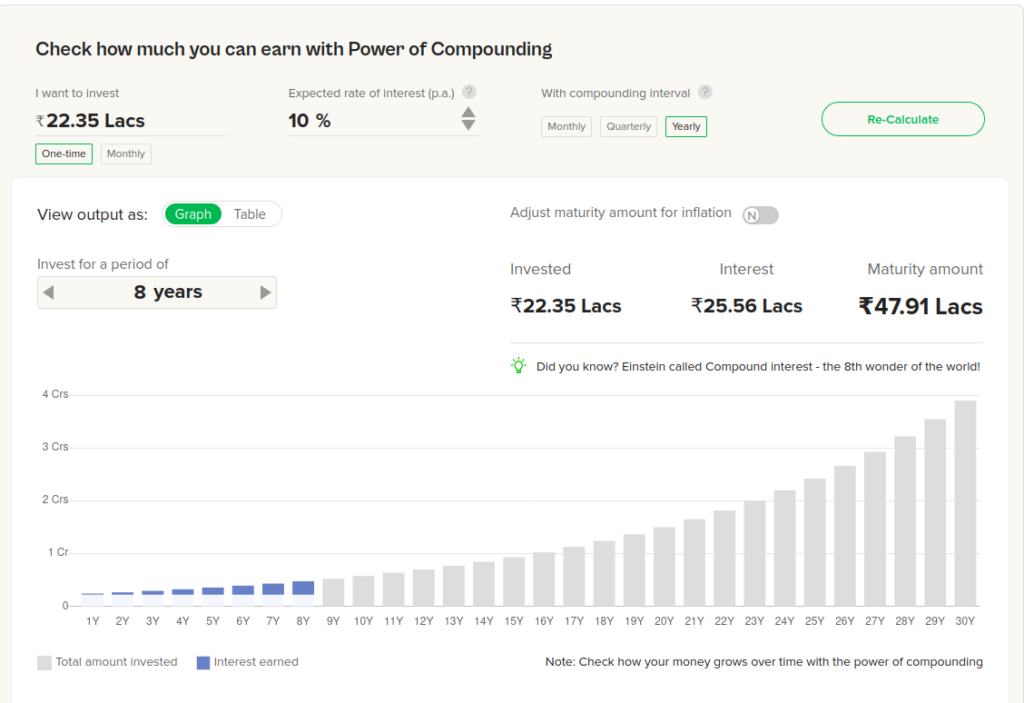

Compound this value of 22.35 lacs for 8- years at 10% interest, and you will get 47.91 lacs.

There is a stark difference of 17 lacs just for making your returns, so-called assured returns.

Even a return rate of 8% is still better than this plan.

You can apply the same concepts to ULIP plans, Term Insurance Plans with Return of Premiums, and other endowment plans.

But before concluding, I still want to reiterate this article is based on my personal views, and you should do the logical calculations and make the right decision.

Your plans may offer different benefits, perhaps even better, and maybe it makes sense at that time. My whole purpose is to help you make better decisions and learn the applications of the functions and formulas, not get swayed by the sweet talks of insurance agents.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.