Skip to content

Skip to content

How to Invest 1 crore for Monthly Income

Imagine you found your hands on 1- crore rupees and, being an avid reader of personal finance, you plan to invest it for a better future. You begin to think of various instruments and lay out a scheme to get the best of it: how to invest 1- crore rupees for monthly income.

In this article, you will come across one such idea, which is simple and can apply to a greater audience.

Qualities of Our Asset:

There are certain kinds of qualities I want in my instrument at any cost to execute the plan.

The following are:

- Guaranteed Income: Your whole objective is to have monthly earnings. So, choosing instruments that can guarantee income should be our priority.

- Little to no time needed to manage money: Not everyone is aware or has an understanding of the financial market. There are instruments where you can earn great returns by increasing your risk exposure, but it’s not for everybody. Any investment that acts like a cash cow and does not demand maintenance time is a great asset.

Join our Mailing list!

Get all latest news and updates.

- Little to no effort required: Your intention behind having the monthly income is to enjoy the returns. Chasing higher returns by trading more of your energy is not viable, especially if you are in your 50s and 60s. So, our ideal asset will be the one that will need less effort from our end.

- Stay invested for a long tenure: Finding the asset that stays for a long duration in the market is a rule of thumb. If you have to reinvest all your money again and again, after every few years, it will suck a lot of mental energy, and let’s be honest, we are lazy fellows. We want things to be simple and uncomplicated.

- Ease of availability: This one is self-explanatory. The asset should be available to a larger audience to become easy to invest in.

- Taxation: Whatever our earnings, it should attract as low a tax as possible.

All of this ensures that you get the maximum returns out of your money and enjoy the returns without the tension of its safety.

Different Assets to Invest In:

Numerous assets are readily available for us to invest in. But remember our crucial point: We should be able to earn monthly income from it. It is our priority. Even though many instruments can give way higher returns in real life, you need to stay invested in them, and you cannot touch your money.

Some of the available instruments are:

- Real Estate

- FDs

- Equity

- Bonds

- Guaranteed Income Schemes.

Let’s break down each of these instruments for better understanding.

1) Real Estate

Real estate is one of the favorite instruments, especially in India. Everyone aspires to become a property owner someday or another. Real estate is a tool for earning monthly income. You rent out the flat to someone, and they pay you back each month. Let’s see how much it satisfies our requirements.

- Guaranteed Income: You receive rent as long you have a tenant, and sometimes, it is hard to have the property remain occupied. It is a problem if you rely on the rent to meet your needs every month. Moreover, if the complete market falls, your rent will also diminish.

- Little to no time: Everybody knows it; finding the right property is never a cakewalk. To find the right property, you spend a lot of energy and mental capacity to find the ideal property for you.

- Little to no effort: This never happens in real estate. You always look after the property and maintain it to attract better customers. It could be viable for some, but people in retirement would refrain from such investments. It is an option that consumes too much energy.

- Stay Invested for the long term: Real estate is a prime instrument to remain invested for a lengthy period. In this regard, this instrument suits our requirements.

- Ease of availability: Real estate is no game. You need not have the right property in your neighborhood to buy it. So in this regard as well, this does not satisfy our requirements.

- Taxation: Buying and selling a house burns a big hole in the pocket. The rental income gets added to your regular income, but when you sell it, you pay a whopping 20% tax on the profit.

Apart from this, we also have to calculate the returns on the rental opportunity:

Take up the property prices and rents from your region and discover the returns. Divide the total rent by the total cost of the house to find the yield or annual return.

For example, in my area, a 1- Crore flat would provide an annual rent of about four to five lacks annually. So, the returns are somewhere between 4-5% annually. But for regions like Bangalore, the returns are far better. So where you live also becomes a contributing factor to your decision. Remember, these are the maximum earnings you can earn via rent. Also, think about the attributed cost of maintaining an apartment, which will reduce your possible profit.

Next up on our list is Fixed Deposits or FDs.

2) Fixed Deposit:

First thing, the returns of any FD are as follows ( as per the latest reports). An investment of 10 years will provide a 6.5ish rate of return. But when you want to withdraw money every month, the returns may diminish. Now let’s check whether it satisfies our parameters:

- Guaranteed Income: You can take out the money until the bank remains in business. And no bank is safe from bankruptcy. Moreover, only amounts up to 5- lacs get insured under the rule of the Government of India, so if anything were to happen, you cannot claim more than this amount. In this case, FDs are not a safe instrument to provide guaranteed income.

- Little to no time: Creating an FD is not time-consuming. After you decide on the desired tenure and the return, you can open your FD in seconds.

- Little to no effort: You can create a sweep-in Fixed Deposit. Sweep-in FDs can have varied interest rates, and you have to check with your bank for exact returns, but one thing to note is that you have to take out money from your FD every month, and it causes a bit of friction. You want an instrument with minimum intervention and safe returns.

- Stay Invested for the long term: FDs have the highest duration of 10 years. In my opinion, it is not that bad. You can easily create new FDs after every 10- years. In this parameter, it is good to go.

- Ease of availability: FDs are available to anyone having a bank account. Ease of availability is not an issue.

- Taxation: Earnings from FDs are considered your income and get taxed according to your income slab. Moreover, if the interest earned is more than Rupees 40,000 in a year, 10% of TDS is deducted by the bank. It reduces the amount you can spend for yourself, and you go through the tax filing process to claim it.

3) Equities:

The instrument for investment up for discussion is equities.

Equities are the type of investment where you take ownership in any public company. You become its partial owner. As the company valuation increases, so does the price of your investment. Let’s check how much it suits our requirements:

- Guaranteed Income: Nobody can guarantee how much you can earn in equities. You can 10x or even 100x your money but also make a loss on your investment. Moreover, you stay in the market for a lengthy duration to get any large corpus. You cannot touch the funds before that. Because of this, equities do not satisfy this criterion.

- Little to no time: Choosing equities is time-consuming. To prevent future problems, you choose the stocks to invest in carefully.

- Little to no effort: You read many items to choose the right company. Many things are there for you to learn and make informed decisions.

- Stay Invested for the long term: To get the best out of equities, you stay invested for a lengthy period. You earn the highest return on this asset, but these returns are not monthly.

- Ease of availability: Equities are available to anyone having a demat account. It’s not a big deal to open any demat account.

- Taxation: Earnings from equities is one of the simple taxation policies. If you make gains on stocks you sell after a year, you pay a 10% tax on the profit. And if you sell the stock for less than a year, you pay flat 15%.

4) Bonds :

Now, we will talk about the investment instrument referred to as bonds.

Bonds are a type of debt instrument that ensures a periodic payment, either monthly, quarterly, semi-annually, or annually, to the lender. Every organization, big or small, uses this method to raise funds for its operations.

Let’s see how much of the criteria it fulfills:

- Guaranteed Income: The bond owner receives the payment in a timely fashion. The owner receives compensation automatically according to the decided interest rate and does not have to do anything extra.

- Little to no time: You don’t have to invest any time once you buy the bond. You enjoy the frequent payments to your bank account.

- Little to no effort: Some effort is required to choose the right kind of bond for you and your family. Some of the bonds do not consume much energy, like the government bonds, which have the guarantee of the government.

- Stay Invested for the long term: Bonds have a varied tenure. Some can be 2-5 years, but some bonds, like the government bond, can go as long as 30 years.

- Ease of availability: Bonds are available to anyone having a demat account. It’s not a big deal to open any demat account.

- Taxation: If you sell after a year, you pay a 10% tax on the profit. And if you sell for less than a year, the tax is according to your slab rate.

5) Guaranteed Income Schemes:

The instrument for discussion now is the Guaranteed Income Schemes:

In this scheme, you invest your money according to the investment plan and receive monthly or annual payments after a certain period, say 15 or 20 years.

I would not go in-depth about why these types of investments are so bad. You can check one of my previous articles, where I have explained in detail why this option is only safe when you purposefully want to lose your money.

How To Invest 1 Crore Rupees

After reading about all the possible avenues of investment, the best asset would be bonds. There are various bonds, but our preferred bonds will be government bonds.

Government bonds are debt taken up by the Governments to build essential facilities such as roads, infrastructure, and power plants. They take up money from their citizens and promise them to pay at regular intervals. The government that issues the bonds guarantees the payment. Thus, the risk of the bond getting defaulted is zero.

These bonds are of different periods and go up to 30-40 years, ensuring regular payments.

The Mathematics Behind the Bonds:

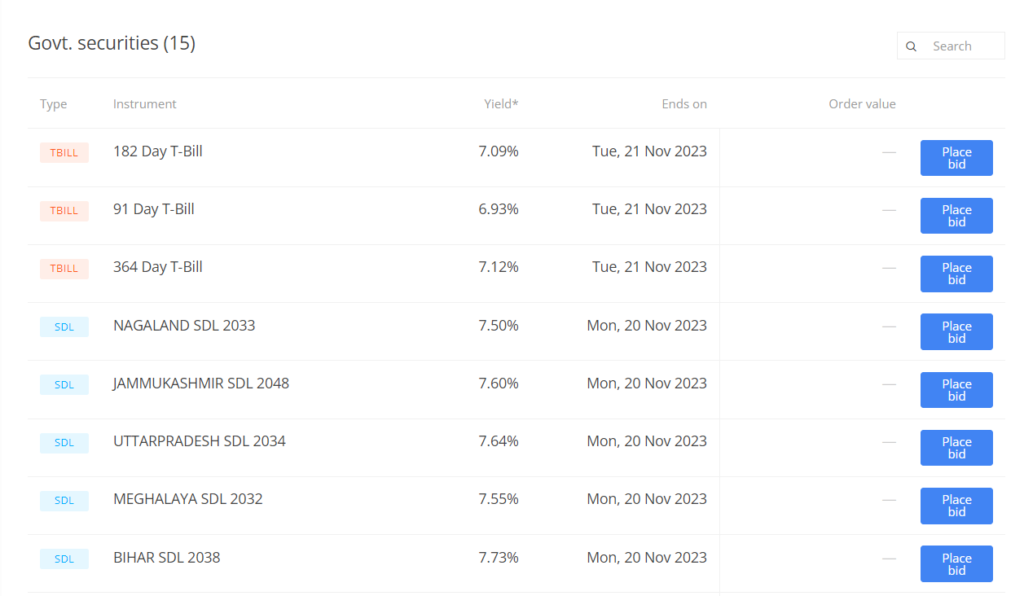

Let’s say we invest our money into government bonds. Let’s see what are the available options. To check the available bonds, you can log in to Kite Coin and see the available bonds.

Let’s take the one with a 7.5% coupon rate:

So when you invest your 1- crore rupees, you will get 7.5 lacs annually or 63K a month. Having 63K monthly in your bank account puts you in the top 10% of Indians.

This kind of money is sufficient to live a stress-free life and spend time on things you want.

Let’s see how it plays out according to our requirements:

- Guaranteed Income: Check. You will receive payments as long as you possess bonds. The longer the duration, the more events of getting paid.

- Little to no time: The government of India bonds are among the safest bonds you can buy in India. If the interest rates satisfy your appetite, it is okay to invest without any more thinking.

- Little to no effort: Government bonds are among the safest bonds. You need not do much research to decide whether your money is safe.

- Stay Invested for the long term: Government bonds can go as long as 30 years. Once you invest, you need not worry about it.

- Ease of availability: Bonds are available to anyone having a demat account. It’s not a big deal to open any demat account.

- Taxation: If you sell after a year, you pay a 10% tax on the profit. And if you sell for less than a year, the tax is according to your slab rate.

On all the parameters, our government bonds suit our objectives. Now, let’s understand how to deploy our cash in these instruments.

Distribution of Funds:

The way we can invest our money is by dividing the money into two segments. 80- lacs and 20 lacs.

I have two reasons for this that I will explain shortly.

As I mentioned, the maximum benefit or gain you can ever achieve in the financial market is via equities only. So, not to deviate from our main objectives, we will set aside a small portion, in our case 20 lacs, to invest in equities.

The power of compounding will help you earn much more than any other instrument.

The other 80 lacs will be divided into 12- parts, where we will invest the money every month into the government-issued bond. This extra work is only for the first year because, after that, you will only need to relax and enjoy the interest payments.

The reason for this is that the interest is paid annually or semi-annually. If you invest all at once, you will receive all your interest earnings once a year, and when you receive a large payment all at once, sometimes it becomes difficult to think straight. You are more likely to spend the money on unwanted things. If you feel that’s not the case, you can invest it in one go.

Join our Mailing list!

Get all latest news and updates.

The other strong reason is when you invest 80 lacs in government-issued bonds at a 7.54% interest rate, you receive a total of 6 lacs rupees Or 50K every month.

The reason I am suggesting you invest a lesser amount is because the interest you receive is counted as your earnings or income, and you have to pay income tax on that according to your slab. According to the new income tax rule in India, if your earning is less than 7 lac rupees annually, you don’t have to pay any tax. So, why not exploit this?

Yes, you are getting 13K less a month had you invested the whole, but you would have to pay tax on that, and the 20 lacs we have set aside is poised to earn much more if you remain invested in equities for the long term.

One part I haven’t answered is where in equities do I need to invest and do I need to invest. I have written a few separate articles on that topic, if you want to know more about it, you can visit the article where I explained the instrument to invest your equities.

Food For Thought:

There is a thought you might wonder. “This all looks good for the person in their retirement age. But what if we get our hands on this kind of money in the early 30s? Will it make sense then also? You might already be in the 20 or even 30 percent tax bracket, does that make this plan viable for me?

The answer is Yes. And the magic word is CASHFLOW.

Conclusion:

Bonds can be a great source of income for all kinds of people. If your needs are met with the amount of interest being paid, then it becomes one of the easier modes to take control of your time and spend time on building better things not worrying about whether you’ll be able to feed your family or not.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.