Skip to content

Skip to content

Saving for a rainy day: How an Emergency Fund can help you Achieve Financial Freedom

Welcome to the next stage of building your wealth. In this article, we will learn about the importance of Emergency Funds and how it prevents you from falling into a debt trap.

If you have not read the previous articles of this series, you can read them here.

If you remember the Pot Story, when you were moving from one place to another part of the country, you took a little precaution.

You stored some extra water in the pot, which you will consume while you and your family are on the journey.

But why?

What was the need for doing this? Why didn’t you pack your bags one day and start your journey?

You were aware that when you and your family are moving from one place to another, you will not be able to find new water sources, and thus it would be better if you have some surplus for this purpose.

This section of the story states the importance of having emergency funds in real life. If there is even a little possibility that the inflow of money gets impacted, it is of utmost importance that you create some surplus for this moment so that at least your basic needs are taken care of by the funds. Keeping an emergency fund is like securing your future self from any unwanted circumstance, and it gives birth to one of those moments where you thank your past self for such a wise decision. Having emergency funds lets you do things with a calm and relaxed mind because there is no immediate requirement to take any decision in haste, which could be problematic for the future.

Sometimes a decision of haste could lead you directly into a debt trap where you borrow some money to pay for basic needs, but the thing is, you would have to pay interest on that. Paying interest just for your basic needs is foolish in itself. If you go on to borrow money every time you buy essentials, then your financial journey will be in a lot of trouble.

Benefits of Emergency Funds

Many day-to-day common incidents signify the benefits of emergency funds. Some of the benefits are:

1) Low Stress: During an emergency, such as an abrupt job loss, auto problems, or unanticipated home repairs, one’s financial stability is affected, which eventually causes stress.

Without any protection against unexpected events, people take serious risks that could hurt their daily lives. But, by setting up an emergency fund, people can face such unforeseen catastrophes without worrying about their finances.

2) Avoiding Bad Debt: People wouldn’t have to decide to use debt, like high-interest credit cards, to cover their requirements if they had an emergency fund. Using this type of debt might result in oversized payments due to added interest, fees, and overall higher penalties due to your reckless activity. To visualize this, you can go backward to the era of Covid, where for 2-years, there was no source of income for many individuals. Everything came to a halt. Nobody was able to do anything. Yet people needed the basic and essential items to sustain themselves. Now people who didn’t have any emergency funds would ask for money from their families, relatives, and anyone who could help.

Many would take up loans from the bank to sustain themselves, and without any income, it would be difficult for them to give back the loan with interest. Repeating a similar process would give birth to a vicious cycle where you keep servicing the debt and become unable to provide the basic needs.

Join our Mailing list!

Get all latest news, exclusive deals and updates.

3) Better Saving Behaviour: By establishing an emergency fund, people are encouraged to save and are less tempted to spend money on luxuries like televisions and video game systems. The saved money can be utilized to create better future by investing in equities.

Even if the above-said reason is insufficient for you to build an emergency fund, there are also many other possibilities where you can benefit by having an emergency fund:

1) You are Self-Employed or A Freelancer

It’s crucial to have an emergency fund set up if you are a freelancer or an independent contractor:

1) If you anticipate your contract expiring soon, you should try to increase the amount in your emergency fund.

2) Also, you might want to set aside more money for months when business is slow.

2) Having only one income

It’s crucial to have a sizable emergency reserve if you only have one source of income. It can assist you if the breadwinner becomes unwell or cannot work or if you have an unexpected job loss. You need to have enough money saved for emergencies if you have a single income. After paying off your debt, you can begin accumulating a sizeable emergency fund.

It’s a possibility that you need to raise your emergency savings if you’re starting a family. So whenever you plan to save money, keep this factor in mind.

3) Having Your Own Home:

When you own a home, you are responsible for all maintenance and repairs. You should set up a sinking fund to pay for renovations and repairs. You might incur unforeseen costs, such as air conditioning or plumbing issues.

Your emergency fund can assist you in handling these expenses and reduce some of the stress associated with house ownership.

4) Last-Minute Emergency

If you live away from home, traveling back home can be pricey, and the expenses rise if you have to leave last minute due to an emergency. In the event of a medical emergency or a funeral, it helps to have a good emergency fund set up to pay for the price of last-minute tickets to go home or visit other family members.

Calculate the price of a plane ticket and other expenses, then start saving money.

Keep in mind that last-minute reservations are frequently more expensive.

5) You are Saving For A Goal

Your emergency fund can prevent you from using your resources for unforeseen expenses if saving towards a goal like owning a home or opening a business. By doing this, you can keep these goals from sliding backward.

While rebuilding your emergency fund may cause a slight slowdown in your forward movement, you can still keep the money you are saving for yourself. Your savings will be well-protected in this way.

You can achieve your long-term financial goals by having an emergency fund.

Consider your emergency savings as a form of insurance against unforeseen costs.

6) Medical Emergencies

You might use up your annual deductibles due to a medical issue. Moreover, you might also need to use up your sick time or have frequent tests that mount up quickly, forcing you to take unpaid leave.

You can manage these expenses and find it simpler to get through these trying times with the aid of an emergency fund.

The cost of medical treatment might be high, and insurance companies might not always pay what you want.

Also, you can miss work and exhaust your sick leave, which could result in more problems. Your emergency fund can assist in balancing this.

Join our Mailing list!

Get all latest news, exclusive deals and updates.

Building Emergency Fund

In this section, we will learn about the steps necessary for emergency funds.

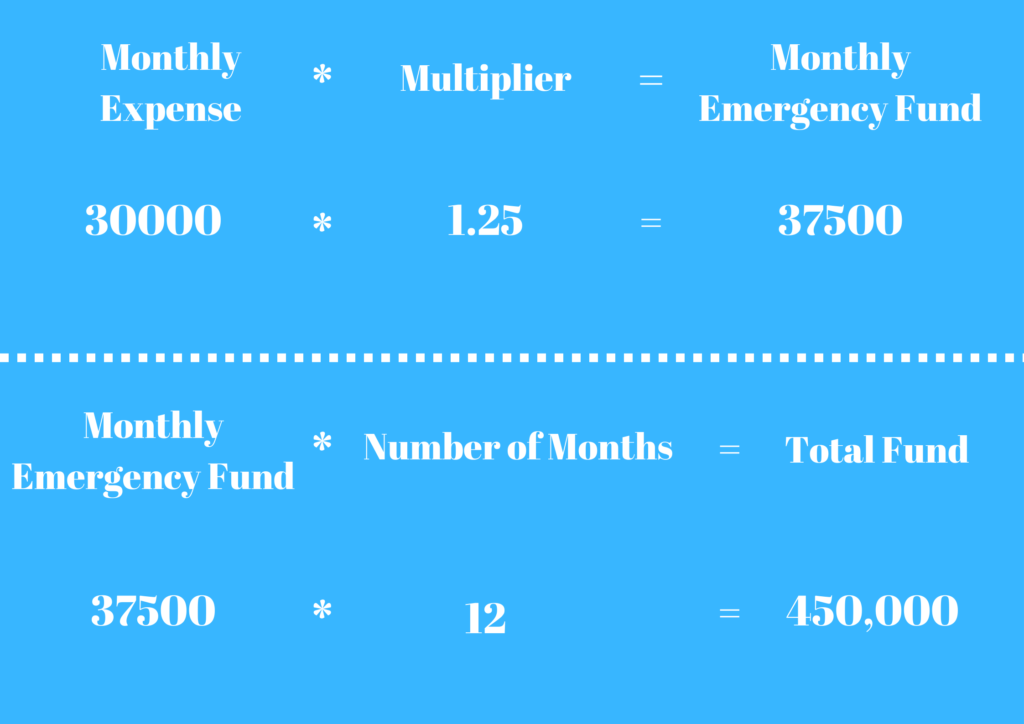

1) Determine your monthly expense:

If you remember from our previous article, we set up a dedicated bank account for your expenditure. That account is the best guide for determining a suitable range of your expenses. Check how much you transfer to your account and calculate a range for yourself.

After getting the desired value, multiply the upper range by 1.25. Why so?

The extra 0.25 is the buffer we take as a precautionary measure.

For example, if your monthly expense is 30,000, then while considering the emergency fund, you should multiply 30,000 by 1.25 to get 37,500.

What you get is the amount you must save for each month.

2) Determine the number of months for your funds:

An ideal range of emergency funds is usually around 6-8 months for salaried employees and roughly 12 months for freelancers and contractual workers.

This usual range of months is self-explanatory. People in a salaried domain can usually find a new job within six months, so saving for 6-8 months is usually a safe number.

An emergency fund can let you prefer a low-paying position until you learn new skills and apply for high-paying jobs. Or if you find that the lower-paying job could provide more free time to start something of your own.

Multiply the single-month expense by your ideal range of months.

For example:

- A salaried Person can have the following calculation: 37500 X 6 = 225,000

- Similarly, for a freelancer, the figure could look something like this: 37500 X 12= 450,000

The calculation mentioned here is just for the basic needs and expenditures. If you have some additional expenses that can crop up, do not forget to consider them.

3) Start building up the funds:

After having all the above-said calculations, there are two ways in which you could build the fund for yourself.

1) Either work towards building the fund to the desired value and then begin investing for more gains.

2) Build up the fund while continuing to invest.

In my opinion, the first choice works far better than the second option as it gives up more security to your finances.

Wherever you put your money, it should fulfill some of your requirements. Investing your money is done to build up wealth for the future, and with the help of compounding, you can achieve your target. But this takes time.

Let’s say after a few months of saving into an emergency fund and investing, you face a situation where you have to use up the funds, and when the emergency funds get exhausted, you will begin to use up the invested amount.

Thus, you were not able to accomplish what you intended by investing.

Instead, had you built your emergency fund first, you wouldn’t have had to dive into the money invested.

4) Choose the right tool:

Now is the time to pick the instruments where you will build up your funds.

There are many popular options where you can choose to save your money.

Some of them are:

a) Fixed Deposit: This is the most sought-after instrument, especially in Indian households. You can open a fixed deposit in any bank and have a surplus of funds read. Moreover, your fund earns money if it is left untouched.

You can allot 50-60% of your funds to this instrument. Or even more; if you are not interested in the below funds.

Remember I recommended you open the net banking service of your income and investment accounts. You can now use this service to set up a fixed deposit without going to the bank. Choose either income or investment accounts and work towards reaching your target. Move the money in the first week of the month after putting aside the money for your expenses.

b) Liquid Funds: These instruments are a mixture of various bonds, which you will learn about in upcoming articles. These bonds have a low-interest rate, depending upon the country you reside. You can invest some funds here for higher returns than fixed deposits.

c) Gilt Funds: Gilt funds are the collection of funds that mainly comprise government bonds. These bonds are usually the most secure as the government rarely goes bankrupt and delivers the amount back to its bondholders.

d) Cash: Having some emergency funds in cash is always a good option. There could be a time when you can’t access money online. Having some hard cash can let you pay for any immediate expenses.

Conclusion

In this article, you have understood the importance of creating emergency fund and how you can build it. Before proceeding to the subsequent article, where we will learn about the importance of insurance, I recommend you at least do the required calculation for a better sense of your requirements.

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.