Skip to content

Skip to content

Boost Your Financial Health: Strategy for Improving Personal Finance and Managing Money Wisely

When you explore the Internet for articles consisting of the keyword Improving personal finance or How to improve financial skills, you will find approximately 982 million articles and supporting material related to this topic.

Such a magnitude of articles speaks for itself about the lacking financial knowledge and the proper guidance for improving personal finance that has been missing in our education.

We are made to learn about the laws of physics and Archimedes’ Principle, but seldom are we taught about the principles of money and money-managing skills that allow us to live our life on our terms.

Money management consists of conservative decision-making, but the current quick rich methods and betting on risky products have often led people to get poor quickly.

To combat this issue, I have created a series of articles designed to provide knowledge in managing and improving personal finances and make you financially secure, if not an affluent millionaire.

So let us start our journey of using our common sense to begin improving personal finance.

Take out a sheet of paper and write down the answer to the following question. Come on, do it. Take a neat piece of paper and carefully answer the below question.

"How much money would you need at this exact moment so that you could pick up the phone and call your manager telling him that you won't be working for him, or matter of fact for anyone, anymore?"

If I put it another way:

You are in your early 20s and do not have a job; the question is even better.

How much money do you need require today so that you don't have to think about getting a job?"

The amount includes everything from marriage in the future to your child’s education to buying your dream house. But only the necessities and practical ones. Do some research. Check out the current price range for your objectives. Think about what would be ideal for you and your future family.

If this question requires you to spend a good half or 1 hour on it, do it.

Be realistic. Do not just write hundreds of crores. Well, you could write it, but then you would need to work according to that goal in a completely different fashion which is beyond the scope of these articles.

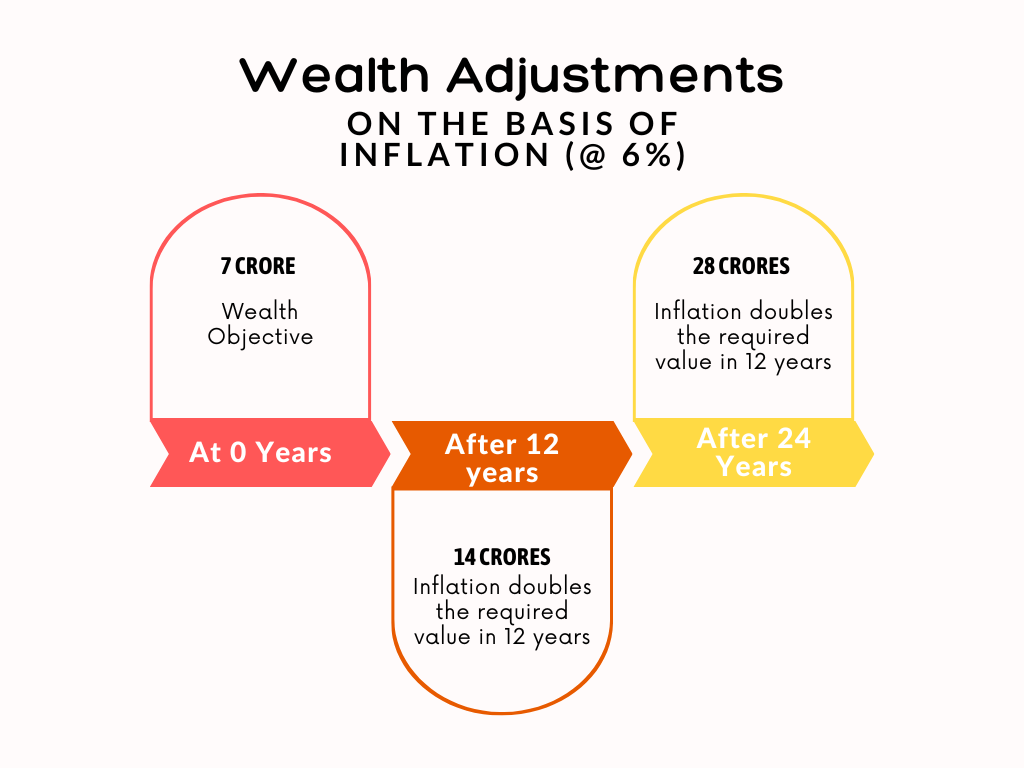

And those of you that have estimated the required money, congratulations. You just took your first step. If I assume the current scenario, especially in India, many readers here will be comfortable with 10-20 crores in their bank account. On the conservative end, I feel even 6- crores are enough if you get it today.

The above image is a representation of my goals. I have mentioned only the important objectives of one’s life for guidance purpose. You can make yours as elaborated as you desire.

Found an approximation? If I can guess, it would be roughly 5-6 crores. If higher or lower, it’s not an issue. Read along with the article.

Now we all know that we aren’t going to get this money in a very instant we would have to work for it, maybe we would need to start a new business or invest more towards improving our skills, and then somewhere down the road, after 8-10 years or maybe more, we could smoothly retire.

But then you might say the current value of money will buy fewer things in the future when inflation kicks in.

And you are right, so before following along, make a quick Google search about the inflation rate in your country. It could be 3% in the US or maybe 6-8% in a country like India, where I live. Found it?

A Cheat Code

Whatever the average rate of inflation, divide 72 by that number.

It is called the rule of 72. This rule expresses the year your money requires to double.

Let’s take the example of India, where it ranges between 5-7%. I will take 6% as my inflation rate. When I do the maths of dividing 72 by 6, I get a value of 12 years. So the value of 7 crores you saw above will double to 14 crores in 12 years.

When you do the maths for yourself, you will get the number of years, after which the amount you require to be financially free doubles.

One thing to note is that this is just an estimation to find a suitable range, not the exact calculation. You cannot always create a perfect strategy every time for yourself. It is not how life works. Maybe the housing market rises so high that the value of real estate skyrockets, making a dent in the whole plan, or perhaps the prices collapse so that I could buy a much bigger house at the same price. Or inflation goes to a highly unacceptable range that your money becomes insignificant. It is not to say that we should not create a plan for it.

So coming back to my own plans, if my basic needs do not change drastically, I need to earn 14 crores if it takes me 12 years to meet my goals from the time I wrote this article. Or if it takes another 12 years, then again, the price doubles up to 28 crores.

So before continuing, make sure you have your own plan.

Before resuming, let’s detour a little and listen to a story. While doing the groundwork for this writing, I wanted something meaningful I could use as an analogy in this and further articles of this series. So I came up with a story titled “A Pot Story.” The purpose of this story is to make the financial requirements presented to you in such a manner that you would easily remember them and follow them. So let’s dive in.

POT STORY

Say you and your family are traveling on foot, and you must pass a barren and desert-like country to reach your destination. You have no other option but to go inside the vast field of sand. It’s not that difficult to survive, but you must be careful.

One thing to remember in the country is you can buy the essentials inside the land using water, but its availability is inadequate. The only thing to do is toil hard to find new water sources so that you can exchange them for other items.

Before entering the city, you find a pot maker. The pot maker has various pots of many sizes and different shapes.

You buy the pot relevant to your use and another one for emergency and start your journey. You find a suitable place for you and your family to rest and go on to find some water sources. As you scour the field, you find little water sources with less water, but seeing a good number, you think it makes sense to take whatever you find and fill the pot.

You bring back some water and fill your pot. You withdraw some to buy food and clothes for your family and your own drinking usage, and you let some remain in the jar for future use, for it will serve when you begin traveling again.

After repeating a similar process for a week, you realize there is enough drinking water for you and your family to travel more distance. Since you won’t be able to look for water sources, it makes sense that there is ample quantity for such a situation.

But then a thought strikes, what if, while traveling, you somehow break your pot?

You could slip, the jar falls to the ground, or some unwanted incident occurs, and all you have is nothing. All your efforts went down the drain.

Join our Mailing list!

Get all latest news, exclusive deals and updates.

You wouldn’t like it. Would you?

So you plan for this and shield your pot by wrapping it with clothes and putting it in a box where it remains protected.

You travel some days, utilizing the water efficiently, and controlling your consumption, so you don’t run out of water. Controlling excess consumption is necessary for this scenario, as not having any water to refill the pot can quickly lead to panic for you and your family.

After traveling some distance, you find a new place to stay put. You begin your journey of finding water sources. You discover some, and you refill your pot. Meanwhile, you find some men, who have a source for themselves, but due to a lack of foresight, they did not secure their pot well enough and broke it during their journey.

Seeing this as a fantastic opportunity, you offer your pot but ask for a tenth of water. This tenth of water proves very valuable as it releases some burden off you. You can take more rest and take care of your health. You could spend time doing some other important tasks for yourself.

This process continues for some weeks, and slowly your pot begins to fill quickly. The extra water could let you buy new things and better services.

As this process continues, you realize that your second pot is also getting filled even though your consumption has slightly increased. This surplus enabled you to finally stop your involvement in the barren land and pass the country without any worries and troubles.

THE END

This story might not feel as valuable yet, but let’s decode the story.

The “Water” in the story is analogous to the actual money in real life. You work hard to earn and exchange it for other goods and services. You use it as per your requirement and let the remainder stay there for future usage in case you can’t find more. The “Water” controls your entire economy inside the land and without it. It becomes challenging to survive.

Now let’s talk about another crucial element: ” The POT.” The first thing you did when entering the barren island was to buy a pot. The pot was an essential element in the story as it held the most important currency for you- The Water. Remember when you bought the jar, there were many options. You chose the one that would satisfy you the best. Many options were more oversized than your pot. You could have bought them, but their size would make you slow down and demand extra precaution.

Therefore, the pot size depicts the wealth you require ( which I am sure you have calculated for yourself by now). You could ask for a bigger pot, hence more wealth, but you must understand you ought to work accordingly and sacrifice much bigger things. And at the end, the only question you have to answer is, ” Is it worth it?” When you have the money you need to retire, does it make sense to go out and fight for more when all it signifies is just more money in your bank account? It doesn’t.

But one thing you definitely would have less is the time which you could utilize for more enjoyable things.

So the first step to improving personal finance is to decide how big a pot you want. This calculation is the foundation of your finances. All future decisions will rely on this. What would be your earning rate, and how fast should you consume to reach your goal? It all depends on how much you want to have. The higher your needs, the more you need to work to achieve that objective.

The other components of the story depict the following:

- Filling up the pots for few days of journey= Creating an Emergency Fund

- Protecting the Pot in the Journey= Buying The Insurance

- Sharing the pot to earn extra water= Learn about Investing

And to top it all off, the journey through the land shows your journey to financial freedom.

In your journey to financial freedom, you take various measures to earn money for your living costs. When your income is sufficient to cover all the expenses without you doing any extra work, you are financially secure.

Moving ahead, one keyword that you must understand to improving personal finance is the word CASHFLOW. Cashflow is the only word that you must master. You can calculate the cash flow using the following formula:

Income – Expense= Cashflow

If your cash flow is positive, you can use the surplus to invest in more things for yourself, but if the cash flow is negative, it denotes either you are burying yourself in debt or; using your investments to pay for your expenses. Both situations are not suitable for you to achieve financial independence.

If you recall the story, whenever you were pouring water into the pot, your consumptions were much less than that. You and your family did not consume everything you found the very day. You saved some for future use, which led to the building up of water level inside the pot. It is a perfect example of positive cash flow.

How To Increase Cash Flow

After looking at the expression closely, you can deduce that you could increase your cash flow by changing to variables.

i) Let income remain constant and reduce expenses;

ii) You increase the earnings and let Expenditures remain constant;

There is another option you might counter with, which is when you increase both revenue and expenses, but the change in earnings is more than the change in expenditure. It is one of the major traps most people fall in. When you do this, the rate at which your cash flow increases becomes less. You have less money to invest, and you fall into the trap of-: lifestyle inflation.

When you think about the first option of reducing your expenses and making your income constant, you could increase your cash flow, but there is a problem. You can only lower your expenditure to a certain level without affecting your basic needs. You can live away from luxury items but not the basic ones. Thus this option is not suitable for the long term.

Now, coming to the next point:

Many of you are already earning, and many young readers will enter the economy to look for new jobs. It will create a constant source of income which you can utilize along the guidelines mentioned in these articles.

You can boost your primary income by upskilling yourself. But I would suggest looking for other avenues and other business opportunities to create new income sources for yourself.

I wrote an article long ago on the importance of multiple income streams, do have a look. I am sure you will find many insights.

Join our Mailing list!

Get all latest news, exclusive deals and updates.

If your cash flow is positive, you can use the surplus to invest in more things for yourself, but if the cash flow is negative, it denotes either you are burying yourself in debt or; using your investments to pay for your expenses. Both situations are not suitable for you to achieve financial independence.

If you recall the story, whenever you were pouring water into the pot, your consumptions were much less than that. You and your family did not consume everything you found the very day. You saved some for future use, which led to the building up of water level inside the pot. It is a perfect example of positive cash flow.

When you have a steady flow with your primary revenue, look for opportunities; you can harness to increase your income.

All set?

After having all this done, create 3-bank accounts for yourself.

Why so?

These bank accounts are required to build up a mechanism for your income and expenses so that you develop a better understanding of your money. A detailed article is attached below, so let’s jump onto it.

Conclusion

Up until this point, you’ve understood about the importance of cashflow for a good financial success. In the upcoming article, you will understand about many more such ideas. So stay tuned!

Have Something to Say or Share on this topic?

Head out to our forum and join other readers to learn more.